Commercial Real Estate Sentiment Steady in Q1 2026 as Debt Availability Improves

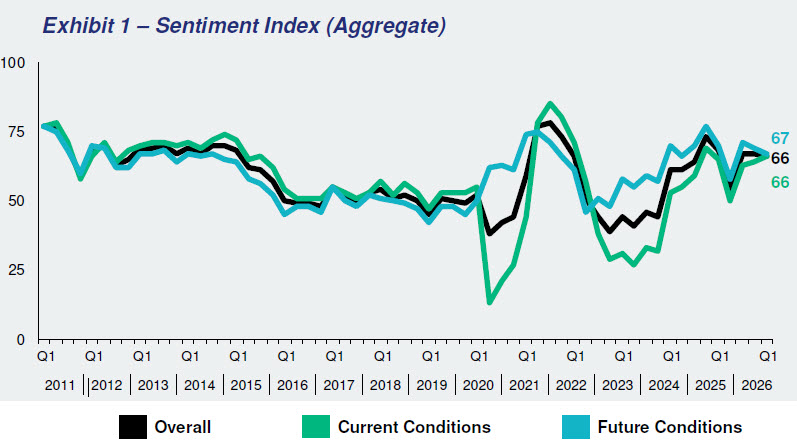

The Real Estate Roundtable (RER) today released its First Quarter 2026 Sentiment Index, a quarterly measure of confidence among senior commercial real estate (CRE) executives. The overall index registered 66, down one point from Q4 2025, as respondents described a market in the early stages of a tentative, uneven recovery. Tariffs and interest-rate uncertainty continue to widen buyer-seller spreads and slow price discovery. (Q1 Report, News Release, Feb. 20)

The Q1 2026 Real Estate Roundtable Sentiment Index registered an overall score of 66, a decrease of one point from the previous quarter. The Current Index registered 66, a two-point increase over Q4 2025. The Future Index posted a score of 67 points, a decrease of two points from the previous quarter, reflecting a prevailing sentiment that the market is in the early stages of a tentative, uneven recovery. Political, tariff, and interest rate uncertainty is contributing to wide spreads between buyers and sellers. Amid the uncertainty around pricing clarity and geopolitical stability, participants are cautiously optimistic for an improved 2026.

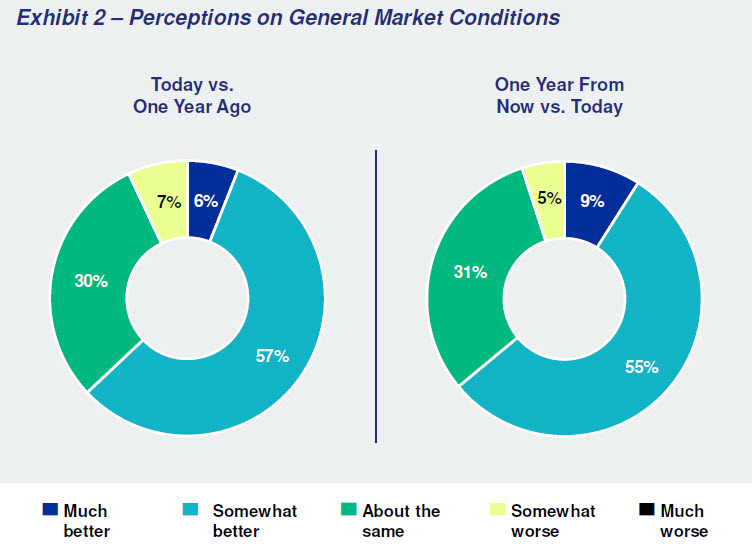

Although perspectives vary by asset class, overall market sentiment trends positive. Less than 10% of respondents believe that general market conditions are worse than this time last year, and 63% believe that general market conditions are better than this time last year. Furthermore, 64% expect general market conditions to show improvement one year from now. Leaders reported strength in data centers and industrial, while returns in the multifamily and office sectors remain heavily location-dependent.

Forty-three percent (43%) of respondents believe asset values are roughly unchanged compared to a year ago. Nearly half of participants are seeing green shoots, as 48% believe asset prices have increased while only 9% believe they have declined. Looking ahead, the outlook is optimistic: 67% expect asset prices to rise over the next year, 30% believe asset values will remain stable, and only 3% anticipate a slight decline.

Perceptions of equity capital availability are muted relative to last quarter, although about four in 10respondents (42%) still believe equity availability is better than a year ago. On the other hand, sentiment around debt capital has risen significantly, with 78% saying the availability of debt capital has improved from last year. Looking ahead, 65% believe equity capital availability will be better in one year, and 49% believe debt capital availability will be better.

Roundtable View

RER President and CEO Jeffrey DeBoer said, “This quarter’s survey shows the market is stabilizing, with improving debt availability and growing optimism about the year ahead—even as uncertainty continues to keep transaction volume below potential.”

“The industry is positioned for a more constructive 2026, but sustained momentum will depend on a stable policy environment,” DeBoer added. “That stability supports investment decisions that drive jobs, housing, and economic activity in communities nationwide.”

Data for the Q1 survey was gathered by Chicago-based Ferguson Partners on RER’s behalf in January. See the full Q1 report.

Capital & Credit

The Fed Signals Capital and Liquidity Reforms as Basel III Endgame Work Continues

The Federal Reserve is moving to recalibrate key elements of the U.S. bank capital and liquidity framework, including Basel III Endgame implementation and targeted mortgage-capital adjustments. The Fed’s Vice Chair for Supervision, Michelle Bowman, signaled this week that reforms should support market liquidity and credit availability while maintaining safety and soundness. (FinancialTimes, Feb. 16)

State of Play

Bowman told bankers at the ABA’s 2026 Conference for Community Bankers this week that the Fed will soon seek comment on two proposals to encourage banks to re-engage in mortgage origination and servicing, within the Basel framework. (Speech, Feb. 16)

Bowman pointed to a “concerning trend” of mortgage activity to nonbanks. She cited data showing banks originated roughly 60% of mortgages in 2008 and serviced roughly 95% of outstanding balances; by 2023, those figures had fallen to about 35% and about 45%, respectively. (HousingWire, Feb.16).

The mortgage capital discussion comes as the Trump administration seeks tools to bolster affordability and credit availability, including directing Fannie Mae and Freddie Mac to purchase $200 billion in mortgage-backed securities. (Reuters, Feb. 18)

“By creating a resilient mortgage market that includes robust participation from all types of financial institutions, we can deliver affordable credit and high-quality servicing to borrowers regardless of economic conditions,” Bowman said. (Speech, Feb. 16)

Bowman said the shift has implications for the banking industry, mortgage market stability, and consumers.

Basel III Endgame

In separate remarks on Feb. 19, Bowman said regulators are modernizing the “four pillars” of the capital framework—stress testing, supplementary leverage ratio (SLR), Basel III Endgame, and the G-SIB surcharge—with a focus on market liquidity and affordable homeownership alongside safety and soundness. (Speech, Feb. 19)

Bowman said the Basel effort is “bottom-up,” not “reverse engineered,” arguing that finalizing Basel III would reduce uncertainty and provide clarity for bank capital standards. (PoliticoPro, Feb. 19)

The Federal Deposit Insurance Corporation (FDIC) and the Office of the Comptroller of the Currency (OCC) recently submitted their Basel-related proposals to the Office of Management and Budget (OMB) for review—an important step in the interagency process. (Reuters, Feb. 13)

The Trump administration regulators have said they plan to rewrite liquidity rules, though details have not been released. (PoliticoPro, Feb. 19)

Bowman’s recent remarks are the clearest signal yet of how the Fed may recalibrate the U.S. approach to Basel capital implementation, following industry concerns that earlier proposals could constrain credit and further shift activity to less-regulated lenders.

Roundtable Advocacy

In December, RER and a coalition of leading business trade organizations urged prudential regulators to examine and modernize large bank capital requirements so they continue supporting consumers, businesses, and the broader U.S. economy. (Letter, Dec. 2)

The coalition letter underscored the negative economic impacts of inappropriately calibrated capital rules, highlighted risks to American competitiveness, and commended ongoing agency efforts to improve the framework. (Roundtable Weekly, Dec. 5)

What’s Next

The Fed is expected to issue the mortgage-capital proposals for public comment before any changes take effect, while agencies continue advancing a revised Basel III Endgame package.

Bowman is expected to testify next Thursday alongside the heads of the OCC, the FDIC, and the National Credit Union Administration at a Senate oversight hearing. (WSJ, Feb. 19)

As regulators advance both targeted mortgage capital adjustments and a revised Basel III Endgame proposal, RER will remain engaged to ensure capital reforms do not constrain credit flows essential to commercial real estate, economic activity, and long-term investment, while protecting safety and soundness.

Menu

Close

Menu

Close