Sentiment Index Shows Market in Holding Pattern as Capital Conditions Improve but Transactions Lag

May 22, 2026

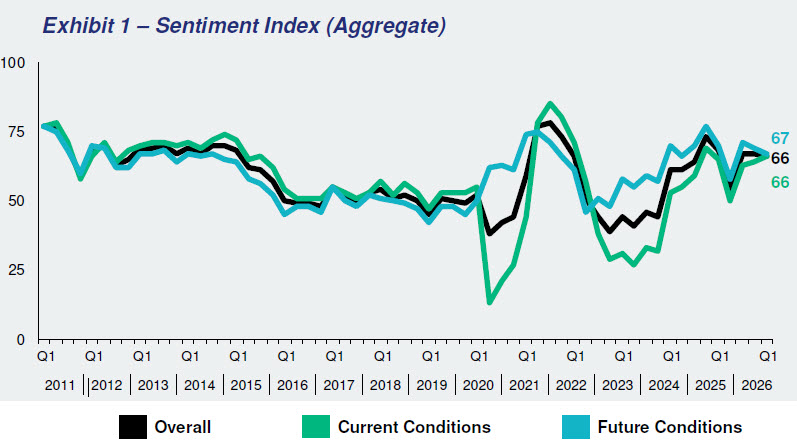

The Real Estate Roundtable (RER) this week released its Q2 2026 Sentiment Index, which registered an overall score of 63, down three points from the previous quarter. The survey shows a CRE market with improving capital conditions and steady fundamentals, but one still constrained by limited transaction activity, pricing uncertainty, and uneven momentum across sectors. (Full Q2 Report)

CRE Market Conditions

The Current Index registered 61, down five points from Q1 2026, while the Future Index posted a score of 64, down three points from the previous quarter. (RER News Release, May 22)

Compared to one year ago, sentiment has improved: current conditions are up 11 points, future conditions are up six points, and overall conditions are up nine points. (Full Q2 Report)

Topline Findings

TheQ2 Sentiment Index's results reflect a market caught in stalemate, where capital is abundant, debt is open, and fundamentals are holding, yet transactions remain stuck behind a wide bid-ask spread. Sellers are refinancing rather than listing, geopolitical shocks have delayed an otherwise visible recovery, and a K-shaped dynamic is widening the gap between well-capitalized players and those running short on equity. The mood is patient, not pessimistic: a ‘decaffeinated’ recovery that participants believe will accelerate once pricing clarity returns.

Beneath the headline numbers, performance is increasingly defined by where firms are and what they own. Top-quartile markets and assets are pulling decisively away from the rest, with industrial, lodging, data centers, and high-quality retail running hot, while multifamily continues to absorb its supply overhang, and office remains sharply bifurcated between trophy assets and everything else. Across every sector, AI is emerging as both a demand driver and an operational force multiplier, reshaping where capital flows and how participants underwrite the next cycle.

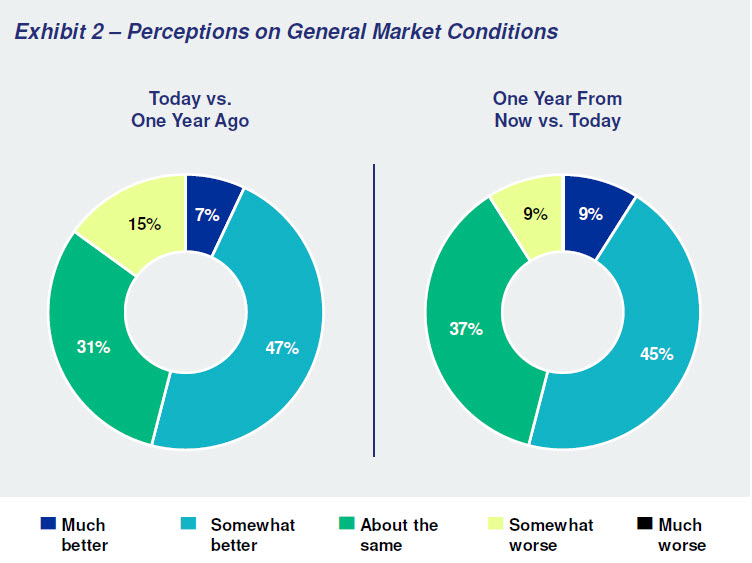

A majority (53%) of respondents believe asset values are relatively unchanged compared to a year ago, while 32% feel they are higher and 15% think values have declined. Looking ahead, the outlook is overall optimistic: 54% expect asset prices to rise over the next year, 37% believe asset values will remain stable, and only 9% anticipate that values will decrease.

Perceptions on equity capital are split, with 24% believing availability is worse compared to a year ago, 33% thinking it is better, and 43% feeling it is the same. On the other hand, sentiment around debt capital is positive, as 69% said the availability of debt capital has improved from last year. Looking forward, 51% of respondents believe that equity capital availability will be better in one year, and 31% believe debt capital availability will be better.

Roundtable View

“Commercial real estate is on stronger footing than it was a year ago, but the recovery is still uneven,” said Jeffrey DeBoer, President and CEO of The Real Estate Roundtable. “Debt is available, values are stabilizing, and fundamentals are holding in many sectors. But transactions remain limited, equity capital is still cautious, and performance varies sharply by market and asset class.” (RER News Release, May 22)

“Now is the time for policies that encourage investment and capital formation—not new barriers that make it harder to build, finance, and modernize the real estate that supports housing, jobs, communities, and economic growth,” DeBoer added.

Data for the Q2 survey was gathered in April by Chicago-based Ferguson Partners on RER’s behalf.

Menu

Close

Menu

Close