Roundtable Comments on Clean Energy Tax Credits for Low-Income Communities, Housing

June 30, 2023

The Real Estate Roundtable submitted comments today on a proposed rule from the IRS and Treasury Department regarding “bonus” tax credits for renewable energy investments in low-income communities, passed by Congress as part of the Inflation Reduction Act (IRA). (Roundtable Comment Letter, June 30)

Taxpayers must apply to the IRS through a competitive process to receive any bonus credits under the Program.

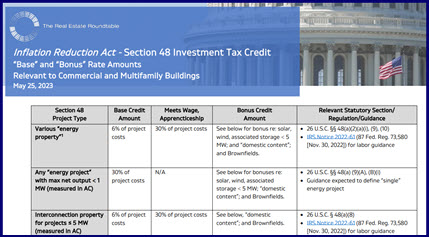

The bonus can provide extra tax credits to help cover the costs of solar, wind, and storage facilities. See The Roundtable’s chart, “Base” and “Bonus Rate” Amounts Relevant to Commercial and Multifamily Buildings (May 25, 2023).

The bonus can increase to an extra 20% for clean energy investments that are part of low-income rental housing—such as housing supported by LIHTCs or Section 8 “housing choice” vouchers.

The bonuses are available only for solar or wind projects that generate under 5 megawatts of electrical output. The Roundtable requested a more straightforward rule for what constitutes a “single project” for purposes of this output threshold.

The IRA’s text requires that multifamily building owners must share “financial benefits” of renewable energy produced on-site with tenants. The Roundtable’s comments stressed that any such benefits should not depend on utility bill savings that accrue directly to tenants—because owners cannot measure, track or control energy consumption in sub-metered leased units.

Low-income housing supported by non-federal programs through state- and local-level housing finance agencies or public housing authorities should also be eligible for the IRA’s low-income bonuses.

The proposed rule would offer a preference, not based in the statute, for non-profit owners to receive bonus credit allocations. The Roundtable’s comments urge there should be no bias against business taxpayers to receive the bonus to further the Biden administration’s climate policy goals for rapid deployment of renewable energy investments in low-income communities.

Future Roundtable comments on IRA topics are in the works. Feedback on a proposed rule to buy-and-sell certain clean energy credits is due August 14. In addition, proposed rules to implement the 179D tax deduction for energy efficient retrofits of commercial buildings are expected this summer.

Menu

Close

Menu

Close