IRS and Treasury Issue Guidance on Opportunity Zone Nominations

The IRS and Treasury Department released new guidance Monday outlining the process for states to nominate census tracts for designation as Qualified Opportunity Zones (QOZs) under the expanded, permanent program enacted in the One Big Beautiful Bill (OB3) Act. (Treasury News Release, April 8)

Proposed Guidance

Treasury and IRS released new guidance establishing the process for chief executive officers of any state, the District of Columbia, and U.S. territories to nominate eligible low-income census tracts for QOZ designation, as well as a list of 25,332 census tracts that meet the low-income requirements. (Treasury dataset | Politico Pro, April 6)

The guidance is a step toward implementing the Opportunity Zone (OZ) changes enacted in the OB3 Act, which made the incentive permanent and expanded it to provide enhanced tax benefits for investments in rural OZs. Rural OZs have lower investment requirements than urban tracts. (IRS News Release, April 6 | Politico Pro, April 6)

Under the statute, states generally may designate no more than 25 percent of their eligible low-income communities as QOZs, subject to special rules for states with fewer qualifying tracts. (IRS News Release, April 6)

The new designations will take effect on Jan. 1, 2027, and future designation rounds will occur every 10 years, replacing the original one-time map established under the 2017 Tax Cuts and Jobs Act (TCJA). (IRS News Release, April 6)

Treasury is developing an online nomination tool to streamline the designation process. (Bloomberg, April 6)

Roundtable Advocacy

Following the passage of the OB3 Act, RER actively engaged Treasury and IRS to support a smooth transition from OZs 1.0 to 2.0, including submitting a detailed comment letter and providing draft guidance for consideration. (Letter, Dec. 19)

RER’s December 2025 comment letter requested urgent tax guidance to ensure investment and capital continue to flow to low-income communities during the transition from the TCJA OZ regime to the new OB3 Act rules. (Letter, Dec. 19)

RER urged policymakers to confirm that contributions to existing TCJA qualified opportunity funds and businesses would continue to qualify for OZ benefits after current zone designations lapse, provided certain conditions are met. (Letter, Dec. 19)

Without clear transition rules, investors could delay or redirect capital, creating unnecessary uncertainty and slowing affordable housing development and economic activity in distressed communities. (Letter, Dec. 19)

OZ incentives have already mobilized more than $120 billion in capital to support housing, retail, and mixed-use development in underserved areas. (Letter, Dec. 19)

What's Next

The QOZs nomination window opens on July 1, 2026 and runs for 90 days, subject to a single 30-day extension. (IRS News Release, April 6)

Treasury and IRS expect to issue additional guidance identifying designated QOZs before the Jan. 1, 2027 effective date. (IRS News Release, April 6)

New OZ designations will run through Dec. 31, 2036, with new nomination rounds occurring every 10 years thereafter. (IRS News Release, April 6)

RER will continue to engage with policymakers to support clear, workable implementation of the new OZ framework, ensure continuity for existing projects, and encourage tax policies that incentivize long-term investment in underserved communities.

Housing

New GAO Data, Rising Cost Pressures Undercut Case for Build-to-Rent Restrictions

As the Senate-passed 21st Century ROAD to Housing Act awaits House action, new federal data and rising development cost estimates are reinforcing a key point in the housing debate: affordability challenges are driven by supply constraints, and federal policy should not make it harder or more expensive to build. (Washington Post, April 6)

What the Data Shows

At the center of the debate is Section 901, which would force large institutional investors to sell certain newly built single-family rental homes after seven years—a provision that could undermine build-to-rent housing and reduce supply. (Roundtable Weekly, April 3)

A new GAO report found that institutional investor ownership of single-family rental homes increased in six metro areas from 2018 to 2024, but still accounted for a very small share of all single-family homes in those markets—ranging from less than 1 percent to 3 percent. (GAO Report, March 24 | Highlights, March 24)

The findings add new weight to the argument that institutional ownership is not the main driver of the nation’s affordability challenges.

The Washington Post noted this week that forcing build-to-rent homes to be sold within seven years would weaken a fast-growing source of new single-family housing. (Washington Post, April 6)

A separate February report from the Progressive Policy Institute (PPI) reached a similar conclusion, finding that institutional investors own less than 1 percent of all single-family homes nationwide and account for less than 2 percent of all home purchases, and concluding that the broader affordability problem is rooted in supply-demand imbalances rather than investor concentration. (Progressive Policy Institute, February 2026)

The reports undercut the argument that restricting institutional investment is likely to meaningfully improve affordability, particularly when housing shortages, financing costs, regulatory barriers, and construction expenses remain the primary constraints on supply.

Market Impact

As Barron’s reported this week, Section 901’s proposed restrictions on institutional investors are already having a chilling effect on investments in single-family housing, with investment managers indicating that pension funds and other large investors may pause or reconsider deals until there is greater clarity around housing policy. (Barron’s, April 7)

Research from John Burns Research & Consulting suggests the Senate bill has “already paralyzed” the build-to-rent development industry, with new development slowing and capital “now frozen,” impacting project viability “from day one, not just in seven years.” (Barron’s, April 7)

Tariffs & Construction Costs

A Joint Economic Committee Democratic report released April 7 found that tariff policy and related uncertainty are exacerbating housing supply challenges, with copper prices up 25 percent year over year in February and steel mill products up 21 percent. (JEC Minority Report, April 7)

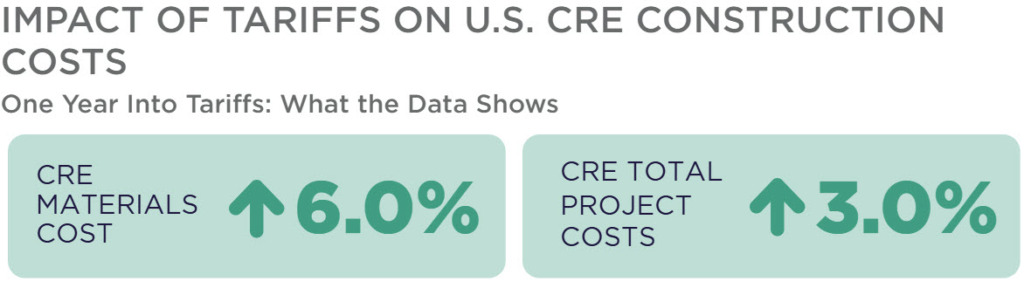

A new Cushman & Wakefield report found that tariff rates in effect as of April 7 would raise construction materials costs by 6.0 percent relative to a 2024 baseline and increase total project costs by roughly 3.0 percent, adding more pressure to housing and commercial real estate development. (Cushman & Wakefield, April 8)

RER & Industry Advocacy

RER and broad housing coalitions have consistently emphasized that housing affordability is driven by supply shortages, construction costs, and mortgage rates—not institutional ownership levels—and that restricting institutional capital would only make it harder to meet the nation’s growing housing needs. (Roundtable Weekly, Jan. 9 | Jan. 16 | Jan. 23 | Feb. 27 | March 6 | March 13 | March 20 | March 27 | April 3) (Letter, March 5 | Letter, March 13)

Research continues to show that restricting institutional capital is unlikely to improve affordability and could create new supply constraints. The PPI report, for example, notes that build-to-rent development is becoming an increasingly important source of new housing supply. (Progressive Policy Institute, February 2026)

What’s Next

Congress returns next week with a robust agenda. The Senate is set to return April 13 and the House on April 14, with unresolved DHS funding, a possible new reconciliation push, and the administration’s budget request all competing for floor time and political attention.

That packed schedule could make it harder for housing legislation to advance quickly.

The Senate-passed ROAD to Housing Act and broader housing policy will be a major focus at the upcoming Spring Roundtable Meeting April 20-21 in Washington, D.C. (Roundtable-level members only).

Menu

Close

Menu

Close