Menu

Close

Menu

Close

Menu

Close

Menu

Close

The Senate’s overwhelming passage of the bipartisan 21st Century ROAD to Housing Act last week has shifted attention to the House, where lawmakers are weighing how to reconcile the Senate bill with the House-passed housing package approved in February. (PoliticoPro, March 17 | Politico, March 19)

State of Play

Executive Orders – Housing

RER & Industry Advocacy

RER will continue urging lawmakers to preserve the bill’s pro-supply provisions while removing language that would reduce rental housing production and chill the capital formation needed to address the nation’s housing shortage.

The IRS and Treasury Department this week issued new guidance allowing real estate companies to withdraw prior elections that had prevented many from fully benefiting from the One Big Beautiful Bill Act’s (OB3 Act) restored 100% bonus depreciation provision. Revenue Procedure 2026-17 outlines how taxpayers may revoke those elections under Section 163(j), clearing the way for broader use of immediate expensing across commercial real estate. (Bloomberg, March 18)

Why It Matters

RER Advocacy

Treasury’s action addresses a key transition issue created by the new law. It helps ensure that restored bonus depreciation can work as intended across a broader share of commercial real estate investment.

The Federal Reserve, Federal Deposit Insurance Corporation (FDIC), and Office of the Comptroller of the Currency (OCC) on Thursday unveiled a substantially revised Basel III Endgame proposal, replacing the 2023 framework that drew broad industry opposition. (WSJ | Fed Board Memo, March 19)

State of Play

Why It Matters

Roundtable Advocacy

The agencies will accept comments on the proposed rules until June 18, and RER's Real Estate Capital Policy Advisory Committee (RECPAC) looks forward to members' input as it prepares comments on the proposal.

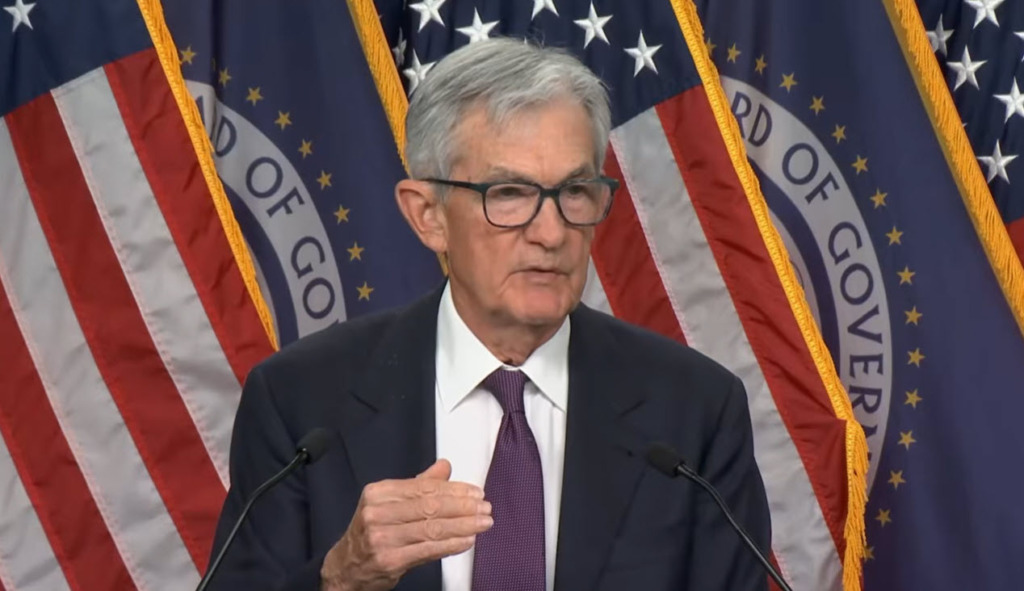

The Federal Reserve's Federal Open Market Committee (FOMC) voted this week to hold its benchmark interest rate steady at 3.5 percent to 3.75 percent, as policymakers weigh persistent inflation, geopolitical risks, and mixed economic signals.

Key Takeaways

Policy Outlook

Congressional Hearing on Fed Independence and Debt Pressures

RER will continue to track monetary policy developments and engage policymakers on the need for stable capital markets, access to credit, and policy solutions that support long-term economic growth and real estate investment.