Menu

Close

Menu

Close

Menu

Close

Menu

Close

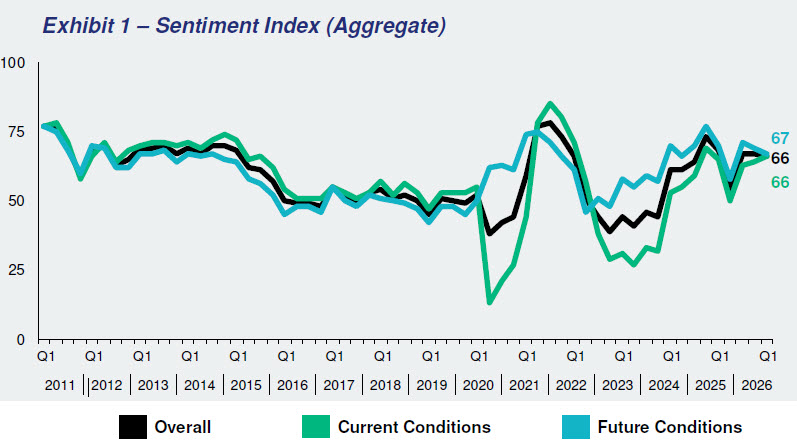

(WASHINGTON, D.C.) — The Real Estate Roundtable (RER) today released its Q2 2026 Sentiment Index, which registered an overall score of 63, down three points from the previous quarter. The survey shows a CRE market with improving capital conditions and steady fundamentals, but one still constrained by limited transaction activity, pricing uncertainty, and uneven momentum across sectors.

Compared to one year ago, sentiments of current conditions are up by 11 points, perceptions of future conditions are up by 6 points, and overall conditions are up by 9 points.

“Commercial real estate is on stronger footing than it was a year ago, but the recovery is still uneven,” said Jeffrey D. DeBoer, President and CEO of The Real Estate Roundtable. “Debt is available, values are stabilizing, and fundamentals are holding in many sectors. But transactions remain limited, equity capital is still cautious, and performance varies sharply by market and asset class.”

“Now is the time for policies that encourage investment and capital formation—not new barriers that make it harder to build, finance, and modernize the real estate that supports housing, jobs, communities, and economic growth,” DeBoer added.

The Q2 Sentiment Index topline findings include:

Sample responses from participants in the Sentiment Index’s Q2 survey include:

“If I had to sum it up in one word, I would say ‘stalemate’. Two years ago, I would have said ‘bear market’–not distress, but some stress.”

“It’s a decaffeinated capital markets recovery. It's there fundamentally, but it’s not allowing for full transactions. It's a rising tide, but there are certainly some ships with holes in their hulls.”

“The top quartile of U.S. markets in each property type are showing a lot more strength than the other quartiles. There's more differentiation in performance across markets, property types, and within sectors.”

“AI is providing tremendous support to the economy. We feel strongly about digital companies investing in hard assets such as data centers, energy generation, storage, and transmission.”

Data for the Q2 survey was gathered by Chicago-based Ferguson Partners on RER’s behalf in April. See the full Q2 report.

The Real Estate Roundtable (RER) brings together leaders of the nation’s top publicly-held and privately-owned real estate ownership, development, lending and management firms with the leaders of major national real estate trade associations to jointly address key national policy issues relating to real estate and the overall economy.