Menu

Close

Menu

Close

Menu

Close

Menu

Close

A bipartisan $79 billion tax package overwhelmingly approved this week by the House still faces potential hurdles in the Senate. The bill contains Roundtable-supported measures on business interest deductibility, bonus depreciation, and the low-income housing tax credit (LIHTC). (Associated Press, and Wall Street Journal, Jan. 31 | The Hill, Feb. 2)

Industry Support for House Bill

Tax Measures Face Senate Scrutiny

Other provisions in the agreement include reforms to the child tax credit, the expensing of R&D costs, disaster tax relief, a double-taxation tax agreement with Taiwan, and a large pay-for that creates significant new penalties for abuse of the employee retention tax credit (ERTC) rules and accelerates the expiration of the ERTC.

# # #

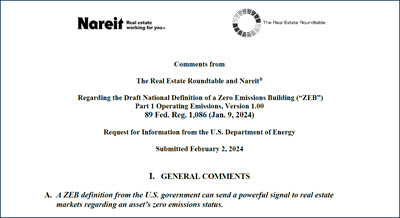

The Real Estate Roundtable (RER) and Nareit submitted comments today to the U.S. Department of Energy (DOE) on its draft definition for Zero Emissions Buildings (ZEB). DOE’s initiative would impose no federal mandates while showing U.S. leadership on climate policy. (Joint comments cover letter and addendum | Roundtable Weekly, Jan. 5)

A “Path to ZEB”

Comments on the National ZEB Definition

Topline points from the RER/Nareit comments (cover letter and addendum) include:

A final ZEB definition is expected later this year. The real estate sector also awaits final climate risk corporate disclosure rules this spring from the U.S. Securities and Exchange Commission. (Roundtable Weekly, Jan. 12)

# # #

On Jan. 30, The Real Estate Roundtable urged the Florida Department of Agriculture and Consumer Services to consider several recommendations on implementing a new law that could have negative consequences for foreign real estate investment in the state. Twenty states have enacted restrictions on foreign investors in real estate or agricultural land, eight states are considering similar measures, and others are exploring the issue. (Roundtable letter)

Restrictions on Foreign Investment in U.S. Real Estate

Roundtable Recommendations

The Real Estate Roundtable’s concerns with Section 204 (692.202) of SB 264 include:

This week’s letter from Roundtable President and CEO Jeffrey DeBoer urged the Florida agency to consider the impact of their interpretation and implementation effort carefully, so that they do not inadvertently prohibit major U.S. investments that are safe from control by foreign countries of concern. Clear legal clarifications to SB 264 can continue to promote safe real estate investment that encourages economic growth without sacrificing the security or economic interests of Florida.

# # #

A group of seven key Democrats from the House Appropriations Committee on Jan. 22 urged Securities and Exchange Commission (SEC) Chair Gary Gensler to exempt real estate assets from a proposed “Custody” rule. The proposal would fundamentally change the ownership and transfer rights of real estate, and impose severe investment limitations on advisory clients. The congressional letter supports The Roundtable’s strong opposition to the rule. (Congressional letter)

Proposed “Qualified Custodian” Layer

Real Estate Exemption

Fed and OCC Voice Concerns

The Roundtable’s Real Estate Capital Policy Advisory Committee (RECPAC) Custody Rule Working Group met with the SEC’s Division of Investment Management last November about the proposal and developed The Roundtable’s comments. Details about RECPAC’s next meeting this spring in New York City are forthcoming.

# # #