The failures of Silicon Valley Bank and Signature Bank this month have raised concerns about the financial health of small and regional banks that hold a large amount of commercial real estate debt—particularly loans backed by office buildings already under pressure from decreased valuations, rising interest rates, and looming debt maturities. (New York Times, March 22 and Wall Street Journal, March 21)

Call for Regulatory Flexibility

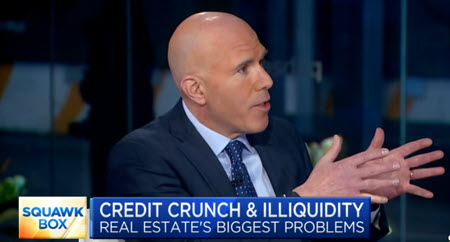

- Roundtable Board Member Scott Rechler, above, (chairman and CEO of RXR) appeared on CNBC’s Squawk Box Wednesday morning to discuss liquidity pressures on CRE. During the interview, he endorsed a recent Roundtable request that banking regulators grant increased flexibility immediately to financial institutions for refinancing loans with borrowers and lenders, allowing time for capital markets to stabilize and the private sector to develop solutions. (Commercial Observer, March 22)

- Rechler added that if no relief is provided, increased pressures on CRE may threaten the tax base of municipalities, the viability of small businesses that rely on regional banks, and the supply of housing. (Squawk Box, March 20)

- Last week’s Roundtable letter from President and CEO Jeffrey DeBoer informed federal bank regulators about the immediate need for reestablishing a troubled debt restructuring (TDR) program for CRE, similar to initiatives established in 2009 during the global financial crisis and in 2020 during the height of the COVID-19 pandemic. (BisNow and GlobeSt, March 21)

- DeBoer’s letter also cited the lingering effects of the global pandemic, including remote work’s negative influence on office space demand, as pressure points on liquidity and refinancing options for CRE assets. (Roundtable Weekly, March 17)

CRE Loan Concentrations

- A March 16 report from Goldman Sachs Research showed that small- and medium-size banks with less than $250 billion in assets account for approximately 80% of commercial real estate lending and 60% of residential real estate lending.

- The Wall Street Journal reported this week that smaller banks hold around $2.3 trillion in commercial real estate debt and that about $270 billion in commercial mortgages held by banks are set to expire this year, according to data firm Trepp Inc.

- Additionally, sales of commercial mortgage-backed securities (CMBS) were down 85% last month compared with the same time in 2022 due to rising interest rates and defaults. (Bloomberg, Feb. 17, 2023)

- Treasury Secretary Janet Yellen testified yesterday before a House Appropriations Committee panel that the federal government is prepared to protect depositors in banks “of any size” who may face the possibility of collapse. “These are tools we could use again for an institution of any size if we judge that its failure would pose a contagion risk,” Yellen said. (Reuters, March 23)

- The Fed is reviewing tougher capital and liquidity requirements for midsize banks, along with more stringent annual stress tests to assess their ability to weather recessionary pressures. New rules may target mid-sized banks with assets totaling between $100 billion to $250 billion. (Wall Street Journal | Financial Times | Reuters, March 14)

The Roundtable’s March 17 letter to federal regulators states, “to avoid increasing unnecessary risk, we respectfully request that the Agencies reaffirm that financial institutions have flexibility to use reasonable and prudent judgment to give borrowers and lenders more time to see properties and loans through this current evolving environment.”

# # #

Menu

Close

Menu

Close

Congressional policymakers this week focused on two tax policy proposals included in President Biden’s FY2024 budget that could adversely affect family-owned real estate businesses—eliminating the step-up in the basis of assets at death and imposing new restrictions on the use of grantor retained annuity trusts (GRATs) and grantor trusts. (Roundtable Weekly, March 10 and Treasury’s “Green Book” description of the President’s revenue proposals, March 9)

Step-up in Basis

Congressional policymakers this week focused on two tax policy proposals included in President Biden’s FY2024 budget that could adversely affect family-owned real estate businesses—eliminating the step-up in the basis of assets at death and imposing new restrictions on the use of grantor retained annuity trusts (GRATs) and grantor trusts. (Roundtable Weekly, March 10 and Treasury’s “Green Book” description of the President’s revenue proposals, March 9)

Step-up in Basis