Menu

Close

Menu

Close

Menu

Close

Menu

Close

Summary

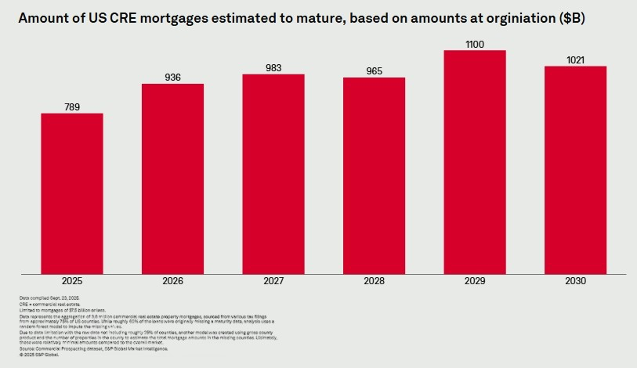

Nearly $983 billion of U.S. commercial real estate mortgages are estimated to mature in 2027. To help rebalance the wave of maturing loans, it is important to advance measures that will encourage additional capital formation and loan restructuring.

As urged by RER, a policy statement—Policy Statement on Prudent Commercial Real Estate Loan Accommodations and Workouts—issued by regulatory agencies encouraging financial institutions to work constructively with creditworthy borrowers on CRE loan workouts is helping to see loans through the current environment. Many of these loans require additional equity, and borrowers still need time to restructure this debt. Capital formation is vital to help restructure maturing debt and fill the equity gap. It is also important to avoid pro-cyclical regulatory actions.

Key Takeaways

Providing banks with the flexibility to work constructively with their borrowers during times of economic

stress has led to billions of dollars of loan restructurings and reduced undue stress in bank loan

portfolios.

The largest U.S. banks’ capital and liquidity levels have grown dramatically since the original Basel III

standards were implemented in 2013 in response to the 2008 Global Financial Crisis. Since 2009, Tier 1

capital has increased by 56 percent and Common Equity Tier 1 capital has tripled. Today, as the Federal Reserve recently observed, the U.S. “banking system is sound and resilient, with strong capital and liquidity.”

See the full fact sheet.

Take a Balanced Approach to Setting Capital Requirements: The re-proposal is viewed by many industry participants as a “pivotal step” toward a more balanced approach for both residential and commercial sectors.

Support Robust Capital Formation: Additional capital is called for to help restructure and transition the ownership and refinancing of commercial real estate from a period of low rates to a time of higher rates. Enacting policies that will encourage robust capital formation is imperative.

Basel III Endgame

Summary

Nearly $983 billion of U.S. commercial real estate mortgages are estimated to mature in 2027. To help rebalance the wave of maturing loans, it is important to advance measures that will encourage additional capital formation and loan restructuring.

As urged by RER, a policy statement—Policy Statement on Prudent Commercial Real Estate Loan Accommodations and Workouts—issued by regulatory agencies encouraging financial institutions to work constructively with creditworthy borrowers on CRE loan workouts is helping to see loans through the current environment. Many of these loans require additional equity, and borrowers still need time to restructure this debt. Capital formation is vital to help restructure maturing debt and fill the equity gap. It is also important to avoid pro-cyclical regulatory actions.

Key Takeaways

Providing banks with the flexibility to work constructively with their borrowers during times of economic

stress has led to billions of dollars of loan restructurings and reduced undue stress in bank loan

portfolios.

The largest U.S. banks’ capital and liquidity levels have grown dramatically since the original Basel III

standards were implemented in 2013 in response to the 2008 Global Financial Crisis. Since 2009, Tier 1

capital has increased by 56 percent and Common Equity Tier 1 capital has tripled. Today, as the Federal Reserve recently observed, the U.S. “banking system is sound and resilient, with strong capital and liquidity.”

See the full fact sheet.