Menu

Close

Menu

Close

Menu

Close

Menu

Close

Summary

In 2023, the U.S. Securities and Exchange Commission (SEC) proposed changes to require SEC-registered investment advisers to put all their clients’ assets, including all digital assets like Bitcoin and certain physical assets like real estate, with “qualified custodians.” The proposal would have required a written agreement between custodians and advisers, expanded the “surprise examination” requirements, and enhanced recordkeeping rules. These rules were originally designed for digital assets. The proposal’s “reasonable” safeguarding requirements are ambiguous as applied to real estate. Furthermore, the SEC’s release contained an inaccuracy regarding the way deeds evidencing ownership of real estate are recorded. RER opposed the proposed rule on real estate and pushed for an exception for real estate.

Following extensive industry pushback, particularly regarding its application to real estate, digital assets, and the high compliance costs for small firms, the SEC issued a notice on June 12, 2025, withdrawing the proposal.

Key Takeaways

The withdrawal of the SEC's proposed "Safeguarding Rule" in June 2025 is a major relief for the real estate industry. The proposal would have categorized physical real estate as a client "asset" requiring a qualified custodian, a requirement industry groups called "preposterous" and "unworkable.”

See the full fact sheet.

Current Regulatory Status

Summary

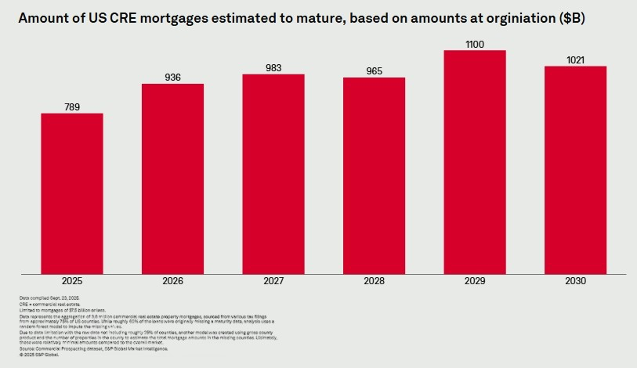

Nearly $983 billion of U.S. commercial real estate mortgages are estimated to mature in 2027. To help rebalance the wave of maturing loans, it is important to advance measures that will encourage additional capital formation and loan restructuring.

As urged by RER, a policy statement—Policy Statement on Prudent Commercial Real Estate Loan Accommodations and Workouts—issued by regulatory agencies encouraging financial institutions to work constructively with creditworthy borrowers on CRE loan workouts is helping to see loans through the current environment. Many of these loans require additional equity, and borrowers still need time to restructure this debt. Capital formation is vital to help restructure maturing debt and fill the equity gap. It is also important to avoid pro-cyclical regulatory actions.

Key Takeaways

Providing banks with the flexibility to work constructively with their borrowers during times of economic

stress has led to billions of dollars of loan restructurings and reduced undue stress in bank loan

portfolios.

The largest U.S. banks’ capital and liquidity levels have grown dramatically since the original Basel III

standards were implemented in 2013 in response to the 2008 Global Financial Crisis. Since 2009, Tier 1

capital has increased by 56 percent and Common Equity Tier 1 capital has tripled. Today, as the Federal Reserve recently observed, the U.S. “banking system is sound and resilient, with strong capital and liquidity.”

See the full fact sheet.