Menu

Close

Menu

Close

Menu

Close

Menu

Close

Summary

The proliferation of natural catastrophe threats has raised concerns about commercial insurance coverage for real estate. These concerns have highlighted the lack of—and need for—insurance capacity and various lines of commercial insurance. Risks from natural disasters like floods, hurricanes, wildfires, hail, tornadoes, and drought cost the U.S. billions of dollars each year. Even if policyholders are able to find coverage for these various lines, prices are increasing dramatically. A lack of adequate coverage will lead to economic uncertainty, harm stakeholders, and undermine the growth of communities.

While commercial property rates are finally stabilizing or even decreasing for high-quality risks, casualty and liability lines continue to face significant upward pressure. Average rates are trending downward by 4.6 percent, with some well-maintained portfolios seeing decreases of 10 percent to 20 percent. A dominant driver for liability lines includes jury awards exceeding $10 million, which have increased by over 300 percent since 2020--particularly affecting the hospitality and real estate sectors.

Spending legislation passed this year has reauthorized the National Flood Insurance Program (NFIP) through Sept. 30, 2026.

RER, along with its industry partners, continues to work constructively with policymakers and stakeholders to address market failure and enact a long-term reauthorization of an improved NFIP.

Key Takeaways

After years of atypical weather patterns and historic losses from natural catastrophes attributed to climate change, economic damages have tripled in cost from just 10 years ago.

Severe storms have surpassed hurricanes as the costliest insured weather peril.

Properties previously considered low-risk are now being re-evaluated due to changes in drainage pressure and local infrastructure.

Due to cumulative construction inflation (up nearly 40 percent since 2020), many properties are currently insured below their actual replacement value.

Commercial property owners continue to take steps to mitigate the risk of natural disasters and potentially lower their insurance costs.

See the full fact sheet.

Enact a Long-Term Reauthorization of NFIP: The level of flood damage from recent storms makes it clear that FEMA needs a holistic plan to prepare the nation for managing the cost of catastrophic flooding under the NFIP.

Increase Private Market Participation: By permitting certain private issue insurance policies to satisfy the NFIP’s “mandatory purchase requirement” for properties in flood plains financed by loans from federally guaranteed institutions, commercial property owners would have the ability to “opt out” of mandatory NFIP commercial coverage if they have adequate private coverage outside the NFIP to cover financed assets.

National Flood Insurance Program (NFIP)

Summary

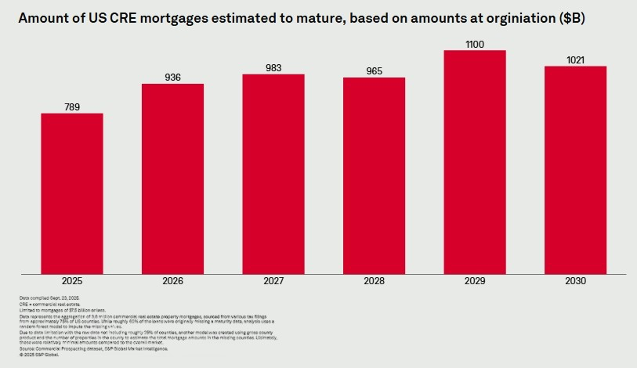

Nearly $983 billion of U.S. commercial real estate mortgages are estimated to mature in 2027. To help rebalance the wave of maturing loans, it is important to advance measures that will encourage additional capital formation and loan restructuring.

As urged by RER, a policy statement—Policy Statement on Prudent Commercial Real Estate Loan Accommodations and Workouts—issued by regulatory agencies encouraging financial institutions to work constructively with creditworthy borrowers on CRE loan workouts is helping to see loans through the current environment. Many of these loans require additional equity, and borrowers still need time to restructure this debt. Capital formation is vital to help restructure maturing debt and fill the equity gap. It is also important to avoid pro-cyclical regulatory actions.

Key Takeaways

Providing banks with the flexibility to work constructively with their borrowers during times of economic

stress has led to billions of dollars of loan restructurings and reduced undue stress in bank loan

portfolios.

The largest U.S. banks’ capital and liquidity levels have grown dramatically since the original Basel III

standards were implemented in 2013 in response to the 2008 Global Financial Crisis. Since 2009, Tier 1

capital has increased by 56 percent and Common Equity Tier 1 capital has tripled. Today, as the Federal Reserve recently observed, the U.S. “banking system is sound and resilient, with strong capital and liquidity.”

See the full fact sheet.