Menu

Close

Menu

Close

Menu

Close

Menu

Close

Summary

The proliferation of natural catastrophe threats has raised concerns about commercial insurance coverage for real estate. These concerns have highlighted the lack of—and need for—insurance capacity and various lines of commercial insurance. Risks from natural disasters like floods, hurricanes, wildfires, hail, tornadoes, and drought cost the U.S. billions of dollars each year. Even if policyholders are able to find coverage for these various lines, prices are increasing dramatically. A lack of adequate coverage will lead to economic uncertainty, harm stakeholders, and undermine the growth of communities.

The budget debate in Congress has called into question the future of the National Flood Insurance Program (NFIP), which is subject to temporary funding extensions. Congress must now reauthorize the NFIP by no later than Jan. 30, 2026.

RER, along with its industry partners, continues to work constructively with policymakers and stakeholders to address market failure and enact a long-term reauthorization of an improved NFIP.

Key Takeaways

The increased frequency and severity of natural disasters is leading to increased premiums for commercial properties.

As economic losses caused by disasters increase, it is important to find new strategies in order to effectively manage natural catastrophe risk.

Expanding coverage gaps and increased costs present challenges for businesses across many industries, including real estate.

Without adequate coverage, the vast majority of natural catastrophe losses are likely to be absorbed by policyholders. These widening coverage gaps and price hikes bring about serious economic concerns about protection gaps, coverage capacity, and increased costs from natural catastrophes and business interruption losses.

Commercial property owners can take steps to mitigate the risk of natural disasters and potentially lower their insurance costs.

See the full fact sheet.

Enact a Long-Term Reauthorization of NFIP: The level of flood damage from recent storms makes it clear that FEMA needs a holistic plan to prepare the nation for managing the cost of catastrophic flooding under the NFIP.

Increase Private Market Participation: By permitting certain private issue insurance policies to satisfy the NFIP’s “mandatory purchase requirement” for properties in flood plains financed by loans from federally guaranteed institutions, commercial property owners would have the ability to “opt out” of mandatory NFIP commercial coverage if they have adequate private coverage outside the NFIP to cover financed assets.

Current Insurance Environment

National Flood Insurance Program (NFIP)

Summary

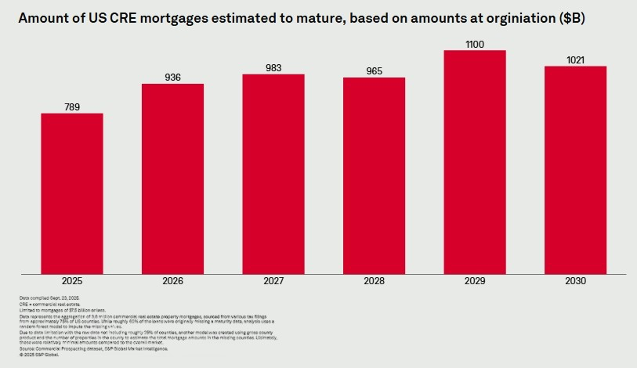

Nearly $936 billion of U.S. commercial real estate mortgages are estimated to mature in 2026. To help rebalance the wave of maturing loans, it is important to advance measures that will encourage additional capital formation and loan restructuring.

It is also important to avoid pro-cyclical regulatory actions such as the Basel III Endgame.

A revised Basel III Endgame proposal announced in September 2024 would have increased Tier 1 capital requirements for global systemically important banks by roughly 9 percent. Concerns remain that any increase in capital requirements will have a pro-cyclical impact on credit capacity and carry a cost to commercial real estate and the overall economy, increasing the cost of credit and constraining capacity. Implementation remains uncertain.

In a January 2024 letter, RER raised industry concerns about the negative impact of the Basel III Endgame proposal, including the higher cost of credit and diminished lending capacity, and requested that the proposal be withdrawn.

Vice Chair for Supervision Michelle Bowman said that the central bank is working with the FDIC and the OCC on reproposal of the rule. A more industry-friendly version of contentious capital rules is expected in early 2026.

In a Dec. 19, 2025 letter to Vice Chair Bowman and other bank regulatory agencies, House Financial Services Committee Chairman French Hill (R-AR) urged regulators to design the Basel III Endgame capital rules in a way that protects bank safety without unnecessarily restricting credit or harming economic growth, while supporting households, businesses, and markets.

Key Takeaways

Providing banks with the flexibility to work constructively with their borrowers during times of economic stress has led to billions of dollars of loan restructurings and reduced undue stress in bank loan portfolios.

The original Basel III Endgame proposalwould have had a significant economic cost without clear benefits to the economy.

The largest U.S. banks’ capital and liquidity levels have grown dramatically since the original Basel III standards were implemented in 2013 in response to the 2008 Global Financial Crisis. Since 2009, Tier 1 capital has increased by 56 percent and Common Equity Tier 1 capital has tripled. Today, as the Federal Reserve recently observed, the U.S. “banking system is sound and resilient, with strong capital and liquidity.”

Further, it is important to bring more foreign capital into U.S. real estate by lifting legal barriers to investment, as well as repealing or reforming the archaic Foreign Investment in Real Property Tax Act (FIRPTA).

See the full fact sheet.