Menu

Close

Menu

Close

Menu

Close

Menu

Close

Summary

Today, the risk of terrorism remains as strong as ever. According to the 2025 Annual Threat Assessment from the Office of the Director of National Intelligence (ODNI), “A diverse set of foreign actors are targeting U.S. health and safety, critical infrastructure, industries, wealth, and government. State adversaries and their proxies are also trying to weaken and displace U.S. economic and military power in their regions and across the globe.”

For more than two decades, at almost no cost to the taxpayer, the national terrorism insurance program established by the Terrorism Risk Insurance Act (TRIA) in 2002 has made it possible for businesses to purchase the terrorism risk coverage they need. Threatened with acts of terrorism, and in the absence of a viable private market, business insurance consumers would be unable to secure adequate coverage without such a program. The Real Estate Roundtable supports a long-term reauthorization of TRIA and urges prompt congressional action to renew this critical program in advance of its expiration on Dec. 31, 2027.

Key Takeaways

Terrorism risk is a national security challenge that requires a federal solution.

TRIA has successfully maintained market stability for over 20 years at minimal taxpayer cost.

Without TRIA, terrorism risk coverage would become scarce or unaffordable, threatening economic

resilience and recovery.

Should a terrorist attack occur without adequate coverage in place, underinsured businesses will face the risk of ruin, with potentially catastrophic local economic effects, and the federal government will face significant pressure to hastily assemble financial assistance to underinsured victims.

Early reauthorization will ensure continued business confidence and prevent market disruption as the

program approaches its 2027 expiration.

It is important to enact a long-term reauthorization of TRIA well in advance of its termination date of

December 31, 2027.

See the full fact sheet.

Reauthorize and Strengthen TRIA: TRIA has been a tremendous success. It is a comprehensive plan to provide for economic continuity and recovery in the wake of a major terrorist attack, while simultaneously protecting taxpayers via a mandatory recoupment mechanism. We urge Congress to promptly enact a long-term reauthorization of this important program.

Terrorism Risk Requires a Federal Insurance Backstop Takeaways

Summary

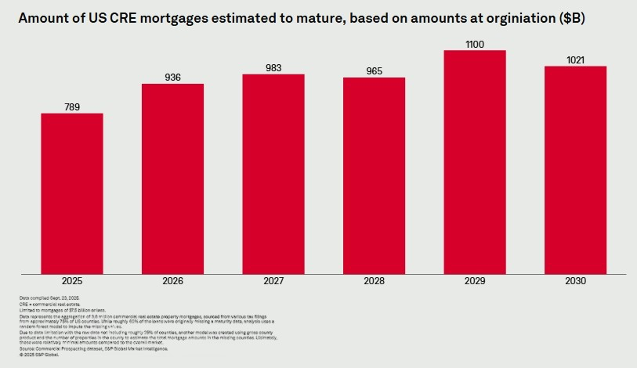

Nearly $936 billion of U.S. commercial real estate mortgages are estimated to mature in 2026. To help rebalance the wave of maturing loans, it is important to advance measures that will encourage additional capital formation and loan restructuring.

It is also important to avoid pro-cyclical regulatory actions such as the Basel III Endgame.

A revised Basel III Endgame proposal announced in September 2024 would have increased Tier 1 capital requirements for global systemically important banks by roughly 9 percent. Concerns remain that any increase in capital requirements will have a pro-cyclical impact on credit capacity and carry a cost to commercial real estate and the overall economy, increasing the cost of credit and constraining capacity. Implementation remains uncertain.

In a January 2024 letter, RER raised industry concerns about the negative impact of the Basel III Endgame proposal, including the higher cost of credit and diminished lending capacity, and requested that the proposal be withdrawn.

Vice Chair for Supervision Michelle Bowman said that the central bank is working with the FDIC and the OCC on reproposal of the rule. A more industry-friendly version of contentious capital rules is expected in early 2026.

In a Dec. 19, 2025 letter to Vice Chair Bowman and other bank regulatory agencies, House Financial Services Committee Chairman French Hill (R-AR) urged regulators to design the Basel III Endgame capital rules in a way that protects bank safety without unnecessarily restricting credit or harming economic growth, while supporting households, businesses, and markets.

Key Takeaways

Providing banks with the flexibility to work constructively with their borrowers during times of economic stress has led to billions of dollars of loan restructurings and reduced undue stress in bank loan portfolios.

The original Basel III Endgame proposalwould have had a significant economic cost without clear benefits to the economy.

The largest U.S. banks’ capital and liquidity levels have grown dramatically since the original Basel III standards were implemented in 2013 in response to the 2008 Global Financial Crisis. Since 2009, Tier 1 capital has increased by 56 percent and Common Equity Tier 1 capital has tripled. Today, as the Federal Reserve recently observed, the U.S. “banking system is sound and resilient, with strong capital and liquidity.”

Further, it is important to bring more foreign capital into U.S. real estate by lifting legal barriers to investment, as well as repealing or reforming the archaic Foreign Investment in Real Property Tax Act (FIRPTA).

See the full fact sheet.