Menu

Close

Menu

Close

Menu

Close

Menu

Close

RER advocates for tax policies that promote capital formation, reward risk-taking, and bolster investment. RER strongly supported the tax provisions in the One Big Beautiful Act (OB3 Act) signed into law in July 2025. The OB3 Act tax reforms, once fully implemented, will spur investment in our nation’s housing supply, strengthen urban and rural communities, and grow the broader economy to the benefit of all Americans.

RER's Spring 2026 Policy Priorities

RER advocates for energy policies that promote a robust supply of affordable power, a safe and reliable grid, and encourage energy efficiency.

RER's Spring 2026 Policy Priorities

RER supports public policy that minimizes regulatory burdens and encourages the availability of credit and the formation of capital while maintaining appropriate systemic safeguards.

RER's Spring 2026 Policy Priorities

Summary

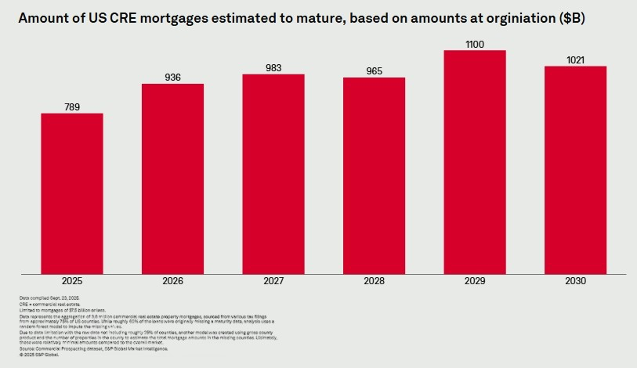

Nearly $983 billion of U.S. commercial real estate mortgages are estimated to mature in 2027. To help rebalance the wave of maturing loans, it is important to advance measures that will encourage additional capital formation and loan restructuring.

As urged by RER, a policy statement—Policy Statement on Prudent Commercial Real Estate Loan Accommodations and Workouts—issued by regulatory agencies encouraging financial institutions to work constructively with creditworthy borrowers on CRE loan workouts is helping to see loans through the current environment. Many of these loans require additional equity, and borrowers still need time to restructure this debt. Capital formation is vital to help restructure maturing debt and fill the equity gap. It is also important to avoid pro-cyclical regulatory actions.

Key Takeaways

Providing banks with the flexibility to work constructively with their borrowers during times of economic

stress has led to billions of dollars of loan restructurings and reduced undue stress in bank loan

portfolios.

The largest U.S. banks’ capital and liquidity levels have grown dramatically since the original Basel III

standards were implemented in 2013 in response to the 2008 Global Financial Crisis. Since 2009, Tier 1

capital has increased by 56 percent and Common Equity Tier 1 capital has tripled. Today, as the Federal Reserve recently observed, the U.S. “banking system is sound and resilient, with strong capital and liquidity.”

See the full fact sheet.

RER supports measures to more effectively address terrorism and criminal threats through a multi-faceted approach involving intelligence gathering, law enforcement, community engagement, and information sharing partnerships, with a focus on prevention, disruption, and prosecution.

RER's Spring 2026 Policy Priorities

RER supports innovative policy incentives that expand the nation’s housing supply and improve housing affordability.

RER's White Paper on Constitutional Concerns in the 21st Century Road to Housing Act: The 21st Century ROAD To Housing Act: A Triple Threat To The Constitution

RER's Spring 2026 Policy Priorities