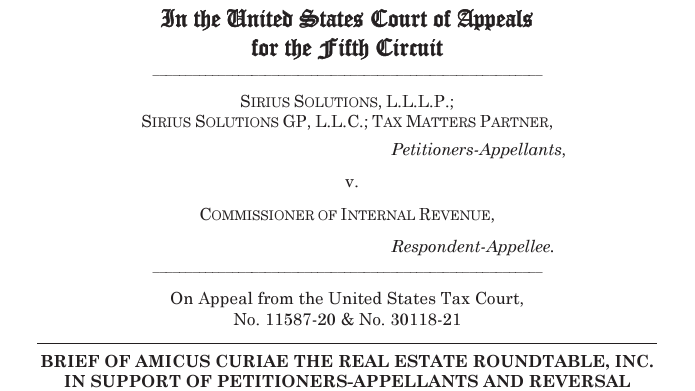

The U.S. Court of Appeals for the Fifth Circuit issued a 2-1 decision in Sirius Solutions, L.L.L.P. v. Commissioner (No. 24-60240) on Jan. 16, restricting the federal government’s effort to extend self-employment taxes to a broad range of limited partners in limited partnerships. The Real Estate Roundtable (RER) submitted an amicus brief in the case, and the Court’s ruling closely aligns with the RER’s position.

Court Ruling

- Since 1977, the tax code has exempted limited partners from self-employment taxes. In recent years, the IRS has asserted a new and more restrictive test to determine whether a limited partner qualifies for the exclusion.

- The Fifth Circuit held that the Section 1402(a)(13) “limited partner” exception from self-employment (SECA) tax applies to a partner in a state-law limited partnership who has limited liability. (TaxNotes, Jan. 27)

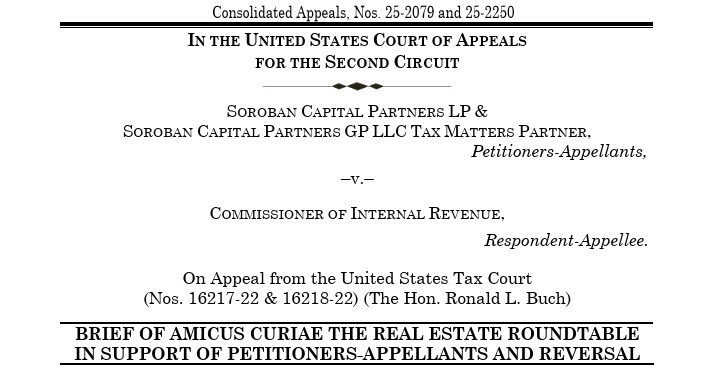

- The ruling vacates and remands the Tax Court decision that followed Soroban Capital Partners LP v. Commissioner (No. 25-2079), and applied a “functional analysis” of partner roles and activities to determine whether the SECA exclusion applies. (Sullivan Cromwell, Jan. 27)

- The Fifth Circuit rejected that approach and held that “limited partner” in Section 1402(a)(13) is a status-based, state-law concept tied to limited liability, not an activity test.

- The decision is the first appellate ruling to reach the issue and reverse the Tax Court’s restrictive interpretation. (Reuters, Jan. 21)

- This ruling has set a precedent for future SECA tax cases, with significant consequences for real estate and other industries that use limited partnerships for business purposes.

Roundtable Advocacy

- In August 2024, RER submitted an amicus brief to the Fifth Circuit. The brief argued that the IRS’s interpretation was flawed and inconsistent with decades of state law recognizing that limited partners can provide services while retaining limited partner status. (Roundtable Weekly, Sept. 6, 2024)

- The brief emphasized that pre-1977 state court decisions and the IRS’s own 1994 proposed regulations contradict the government’s position that limited partners must be passive to avoid SECA taxes.

- RER argued the Tax Court’s “passive investor” test is found nowhere in the statute and reflects a misunderstanding of partnership law that real estate and other businesses have relied on for decades.

- RER has continued this advocacy across the circuits. In Dec. 2025, RER filed an amicus brief with the Second Circuit in Soroban, challenging the IRS’s restrictive interpretation of the “limited partner exception” under Section 1402(a)(13). (Roundtable Weekly, Dec. 19, 2025)

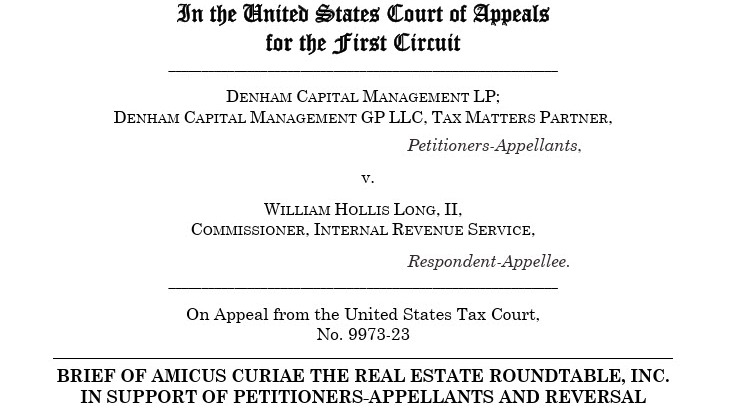

- RER also filed an amicus brief in August with the First Circuit in a related case, Denham Capital Management LP v. Commissioner (No. 25-1349). (Roundtable Weekly, Sept. 12, 2025)

- This successful outcome in the Sirius case supports RER’s position and could reduce momentum for formal tax guidance that would broaden the reach of SECA taxes.

What’s Next

- Related appeals are pending in the First Circuit (Denham) and Second Circuit (Soroban). (TaxNotes, Jan. 27)

- Divergent outcomes could create a circuit split and increase the odds of Supreme Court review. (Skadden Arps, Jan. 27)

- The First Circuit is scheduled to hear oral arguments in Denham on Feb. 5. (TaxNotes, Jan. 27)

RER remains committed to protecting entrepreneurs’ ability to flexibly organize in partnerships and other pass-through entities that promote capital formation, risk-taking, and economic growth, and it will remain engaged as the SECA dispute moves forward.