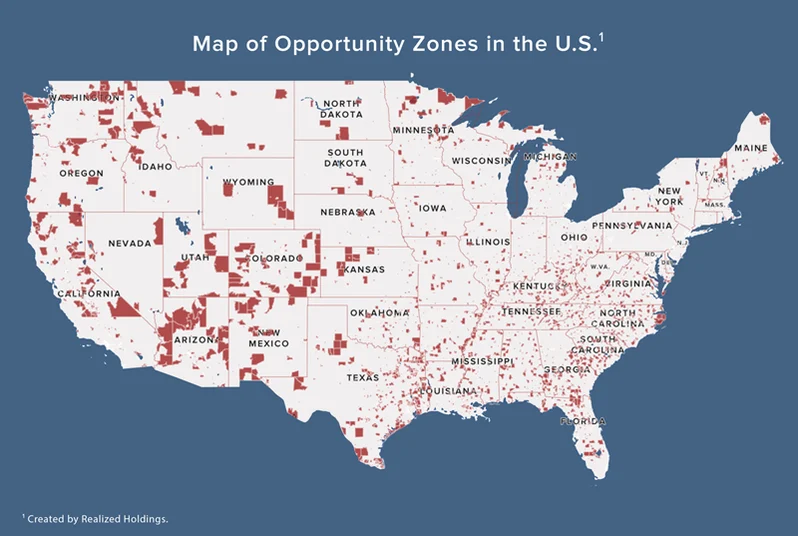

The Treasury Department and IRS issued new guidance last week, IRS Notice 2026-40, providing transition rules for Opportunity Zone investments made or initiated under the original OZ 1.0 regime.

The notice previews rules Treasury and IRS intend to include in forthcoming regulations. It focuses on new OZ designations going forward, transition rules for investors with existing deferred gains, and transition rules for Qualified Opportunity Funds (QOFs) and Qualified Opportunity Zone Businesses (QOZBs) operating in OZs designated under the prior law. (Tax Notes, June 18 | Reuters, June 22)

Why It Matters

- The guidance is a major development for Opportunity Funds and OZ businesses with projects in OZ 1.0 census tracts as the program transitions to the new permanent OZ framework under the One Big Beautiful Bill (OB3)Act.

- While the OB3 Act permanently extended and improved the OZ tax incentives, it left unresolved tax questions affecting investments in expiring OZ 1.0 tracts, including how far along a project must be before a census tract expires and whether future capital expenditures can continue to qualify for the tax incentives.

- The IRS guidance partially adopts a framework proposed by RER that focuses on whether an OZ business has a working capital safe harbor plan in place going forward. (Roundtable Weekly, March 6)

The Notice

- Under the notice, property acquired after Dec. 31, 2026, in a previously designated OZ may still qualify if certain conditions are met. (Seyfarth, June 23)

- To qualify, the OZ business must have a written working capital plan in place by Dec. 31, 2026; future property acquisitions must be consistent with that plan; the business must receive at least 10% of its estimated working capital assets by year-end; and it must expend at least 5% of those assets by Dec. 31, 2026. (IRS Notice 2026-40, June 18)

- The notice also clarifies how OZ compliance tests apply after an OZ 1.0 census tract expires. In certain cases, a previously designated OZ can continue to be treated as a qualifying zone for purposes of the “substantial use” test and the requirement that at least 50% of a business’s gross income be derived from the active conduct of a trade or business in a qualified OZ. (IRS Notice 2026-40, June 18 | Reuters, June 22)

- The guidance provides important certainty for real estate investors, developers, and businesses seeking to move forward with projects in low-income communities during the transition from OZ 1.0 to the new permanent OZ framework.

RER Advocacy

- RER has consistently urged Treasury and the IRS to provide transition rules for OZ 1.0 projects, including through a December 2025 letter, March 2026 follow-up comments, and draft guidance developed by RER’s Opportunity Zone Working Group. (Roundtable Weekly, March 6)

- RER emphasized that unresolved questions surrounding expiring census tract designations could delay projects, discourage new fund formation, and undermine housing production and community development efforts.

- While the notice includes many important details that remain under review, its issuance marks a major step forward in providing greater certainty for long-term OZ investment in underserved communities.

RER’s Opportunity Zone Working Group will review the implications of Notice 2026-40 in the days ahead and continue to engage with Treasury and the IRS to support clear, workable implementation of the new OZ framework.