Menu

Close

Menu

Close

Menu

Close

Menu

Close

Summary

The Corporate Transparency Act (CTA) requires certain companies to disclose information about their beneficial owners to the Treasury Department’s Financial Crimes Enforcement Network (FinCEN). The goal was to create a national directory of beneficial owners to curb illicit finance, drug cartels, terrorist groups, and other harmful activities.

In March 2025, the Treasury Department announced it will suspend enforcement of the CTA for U.S. domestic reporting companies and their beneficial owners, focusing solely on foreign entities. This means U.S. commercial real estate entities are now exempt from providing beneficial ownership information to FinCEN.

FinCEN intends to issue new rules to narrow the scope of the CTA’s reporting requirements to only apply to foreignformed companies that have registered to do business in the U.S.

The Real Estate Roundtable (RER) continues to work with policymakers in support of a balanced approach that would inhibit illicit money laundering activity without the imposition of costly reporting requirements for real estate investors.

Key Takeaways

Treasury’s suspension of CTA enforcement for domestic entities significantly reduces compliance burdens for real estate businesses that rely on LLC structures.

See the full fact sheet.

Support Measures that Encourage Capital Formation: RER, along with its coalition partners, repeatedly raised concerns about the regulatory burden posed by the CTA and has supported the court challenges to the law. We are pleased by the Treasury’s constructive action to exempt domestic reporting companies

CTA Requirements

Summary

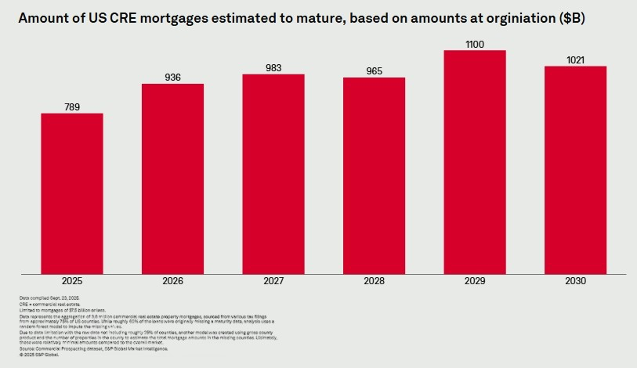

Nearly $983 billion of U.S. commercial real estate mortgages are estimated to mature in 2027. To help rebalance the wave of maturing loans, it is important to advance measures that will encourage additional capital formation and loan restructuring.

As urged by RER, a policy statement—Policy Statement on Prudent Commercial Real Estate Loan Accommodations and Workouts—issued by regulatory agencies encouraging financial institutions to work constructively with creditworthy borrowers on CRE loan workouts is helping to see loans through the current environment. Many of these loans require additional equity, and borrowers still need time to restructure this debt. Capital formation is vital to help restructure maturing debt and fill the equity gap. It is also important to avoid pro-cyclical regulatory actions.

Key Takeaways

Providing banks with the flexibility to work constructively with their borrowers during times of economic

stress has led to billions of dollars of loan restructurings and reduced undue stress in bank loan

portfolios.

The largest U.S. banks’ capital and liquidity levels have grown dramatically since the original Basel III

standards were implemented in 2013 in response to the 2008 Global Financial Crisis. Since 2009, Tier 1

capital has increased by 56 percent and Common Equity Tier 1 capital has tripled. Today, as the Federal Reserve recently observed, the U.S. “banking system is sound and resilient, with strong capital and liquidity.”

See the full fact sheet.