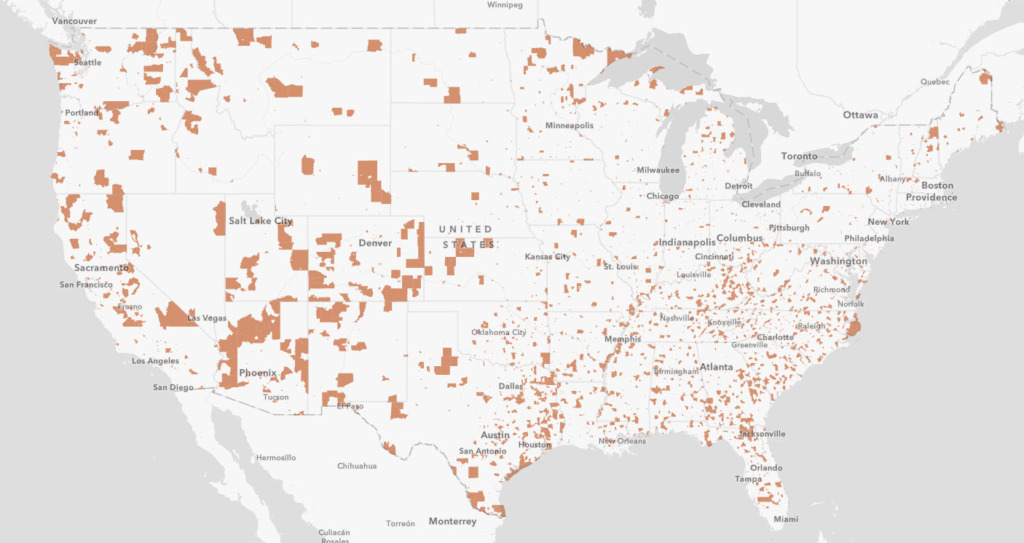

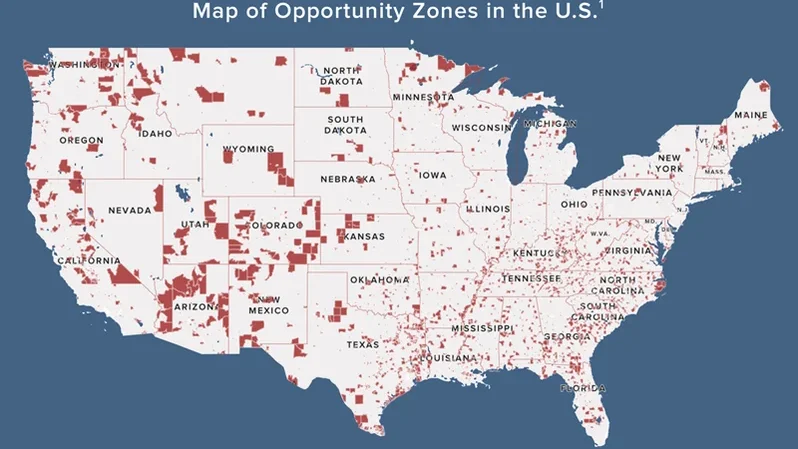

The Real Estate Roundtable (RER) submitted comments this week on IRS Notice 2026-40, welcoming the guidance as an important step in the transition from Opportunity Zones (OZ) 1.0 (TCJA) to the permanent OZ framework enacted under the One Big Beautiful Bill (OB3) Act. RER urged the Treasury Department and IRS to clarify the Notice’s Written Plan and Ordinary Course safe harbors for multiphase investments and allow opportunity funds to continue investing in OZ 1.0 census tracts through their statutory expiration on Dec. 31, 2028. (Letter, July 29)

OZ Transition Recommendations

- The Notice incorporated several concepts previously recommended by RER and has helped unlock capital that had been delayed by uncertainty surrounding investments in expiring OZ 1.0 census tracts. (Roundtable Weekly, June 26)

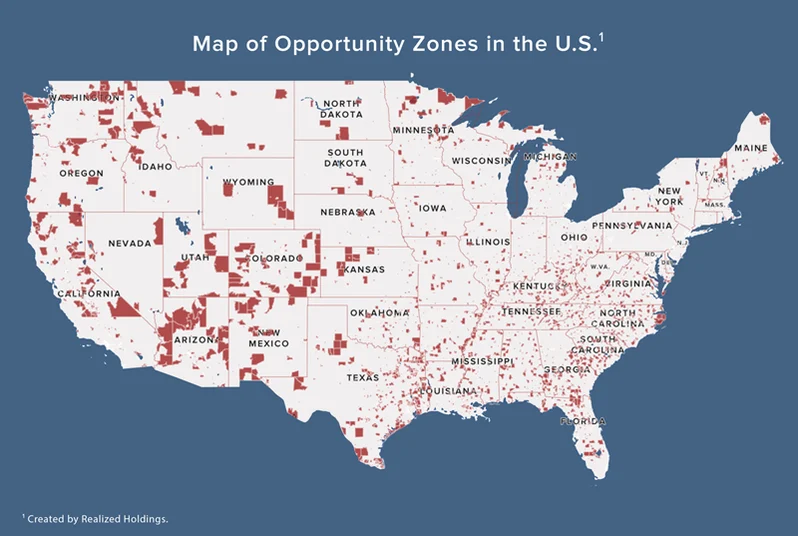

- IRS Notice 2026-40 establishes two exceptions that allow certain investments in OZ 1.0 census tracts to continue qualifying after new zone designations take effect on Jan. 1, 2027. (IRS Notice 2026-40, June 18 | Tax Notes, June 18 | Reuters, June 22)

- Post-2026 investments in OZ 1.0 census tracts must comply with either (1) the “Written Plan” exception, which requires compliance with the existing working capital safe harbor rules and related funding requirements; or (2) the “Ordinary Course” exception, which relates to the purposes of the expenditures (e.g., the permissible modernization or continued operations of the trade or business, as opposed to impermissible expansion of the business or starting a new trade or business).

- RER’s July 29 comments urged Treasury to make both exceptions clear and workable for real estate investors, developers, and entrepreneurs undertaking long-term and multiphase projects. (Letter, July 29)

- Additional clarifications would provide helpful certainty, reduce regulatory risk, and further unlock capital for greater investment in low-income communities. (Letter, July 29)

- Under the Written Plan exception, RER asked Treasury to confirm that capital provided after 2026 does not need to come from the same Qualified Opportunity Fund (QOF) that financed the project earlier and that subsequent phases of an existing real estate business may qualify. (Letter, July 29)

- For the Ordinary Course exception, RER requested administrable rules distinguishing permissible upgrades—such as energy-efficiency measures, accessibility improvements and interior reconfigurations—from business expansions. The letter also seeks clarity for projects involving new floors, conversions of existing space, parking structures, and other improvements that may fall between those categories.

- RER also asked Treasury to allow new QOF equity to fund qualifying ordinary-course improvements, rather than requiring projects to rely on debt, existing cash, or non-QOF equity.

- RER further encouraged Treasury to allow QOFs in OZ 1.0 census tracts to continue investing and acquiring property outside the two exceptions through the tracts’ statutory expiration on Dec. 31, 2028—two years longer than contemplated by the Notice. (Letter, July 29)

- The Economic Innovation Group and Novogradac submitted similar recommendations earlier this month. (EIG Comment Letter, July 10 | Novogradac Comment Letter, July 17)

RER Advocacy

- RER has consistently urged Treasury and the IRS to provide workable transition rules for OZ 1.0 projects, including through a December 2025 letter, follow-up comments and draft guidance submitted by RER’s Opportunity Zone Working Group in March 2026, and meetings with agency officials. (Roundtable Weekly, March 6) (Roundtable Weekly, Dec. 2025)

- RER’s Opportunity Zone Working Group developed the recommendations. Principal drafters included Orla O’Connor and Michael McMahon of KPMG; Gary Hecimovich and Adam Wallwork of Deloitte Tax LLP; Sandy Presant and Jim Lang of Greenberg Traurig LLP; Greg Berger of Brownstein Hyatt Farber Schreck LLP; Angeline Rice and David Sobochan of Cohen & Co Advisory, LLC; Andrea Whiteway of Ernst & Young LLP; and Steven Kennedy of PwC US.

RER’s Opportunity Zone Working Group will continue engaging with Treasury and the IRS to support clear, workable implementation of the permanent OZ framework.