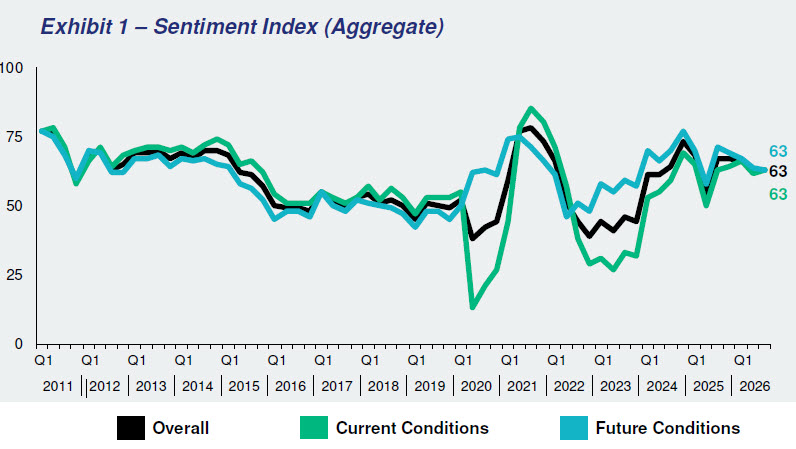

The Real Estate Roundtable’s (RER) Q3 2026 Sentiment Index registered an overall score of 63, unchanged from the previous quarter, as improving property fundamentals and strong debt liquidity were offset by persistent challenges raising equity capital and subdued transaction activity. (Q3 2026 Report)

Topline Findings

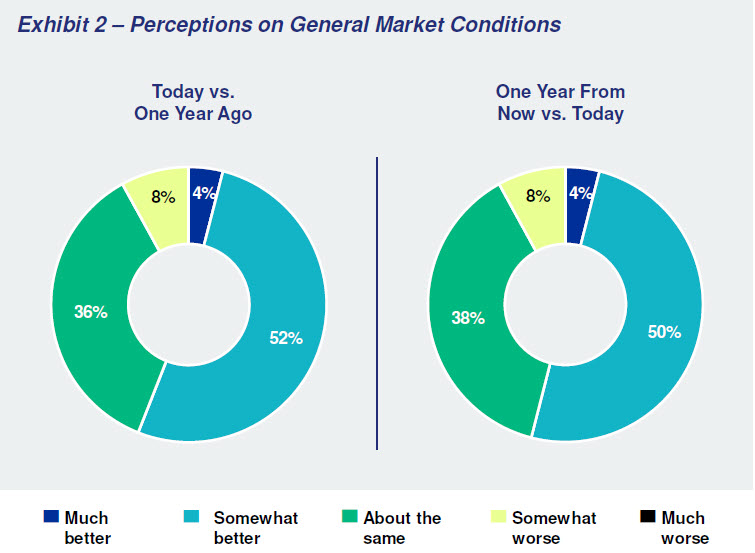

The Q3 Sentiment Index topline findings include:

- The Q3 2026 Index registered an overall score of 63, unchanged from the previous quarter. The Current Index rose 2 points to 63, while the Future Index declined 1 point to 63. (Q3 2026 Report)

- Operating conditions are healthier, but the recovery remains uneven. Improving leasing fundamentals, abundant debt capital, and the stabilization of post-pandemic disruptions are supporting the market. However, fundraising remains challenging, transaction volume remains below desired levels, and investors continue to navigate valuation resets and geopolitical uncertainty.

- Sentiment varies sharply by asset class. Data centers are the clear leader, supported by AI-driven demand, capital inflows, supply constraints, and strong fundamentals. Retail has improved, benefiting from limited new supply and durable demand. Industrial and logistics remain attractive, though enthusiasm has cooled from pandemic highs. Multifamily is more mixed, with long-term demand offset by oversupply and affordability pressures in some markets. Office remains highly bifurcated, as trophy assets and markets gain traction while weaker markets lag.

- Asset values show signs of stabilization. 45% of respondents said values are relatively unchanged from one year ago, 43% said they are higher, and 12% said they have declined. Looking ahead, 49% expect values to rise, 50% expect them to remain stable, and only 1% anticipate a decline.

- Equity capital remains selective. 25% of respondents said availability is worse than one year ago, 35% said it has improved, and 40% said it is unchanged. Half expect equity availability to improve over the next year.

- Debt capital remains widely available. 63% said debt availability has improved from one year ago, while 36% said it is unchanged and only 1% said it has worsened. Looking ahead, 29% expect debt availability to improve further.

Roundtable View

- RER President and CEO Jeffrey DeBoer said, “Commercial real estate fundamentals are improving, supported by stronger leasing, healthier debt markets, and greater stability in asset values. However, limited equity capital and high costs continue to constrain transactions and development.”

- DeBoer added, “Data centers continue to outperform other property sectors, as AI reshapes commercial real estate and drives unprecedented demand for reliable, affordable energy. Policymakers must ensure that energy infrastructure, permitting, tax, and regulatory policies keep pace with this growth. A coordinated approach that expands power generation and transmission, modernizes the grid, and preserves a stable investment environment will help support data center development while protecting ratepayers and meeting the needs of communities and the broader economy.”

RER’s Q3 survey was conducted in July by Chicago-based Ferguson Partners. The Q4 survey will be sent out to members in October.