View Full Report – 2023 Annual Report – Sustained Strength, Sustained Solutions

Tag: Tax Policy

Senate Democrats Propose Tax Penalties on Institutional Owners of Single-Family Rental Homes

A group of eight Democratic Senators introduced legislation on July 11 that would prohibit for-profit owners of 50 or more single-family rental homes from taking depreciation or business interest expense deductions on their properties.

“Short-Sighted Proposal”

- Senate Banking Committee Chairman Senator Sherrod Brown (D-OH), one of the bill’s sponsors, said, “big investors funded by Wall Street buy up homes that could have gone to first-time homebuyers, then jack up rent, neglect repairs, and threaten families with eviction.” Similar concerns were expressed by several cosponsors: Senator Ron Wyden (D-OR), chair of the Senate Finance Committee, along with Sens. Elizabeth Warren (D-MA), Tina Smith (D-MN), Jeff Merkley (D-OR), Jack Reed (D-RI), John Fetterman (D-PA), and Tammy Baldwin (D-WI). (Senate Banking press release, July 11)

- Real Estate Roundtable President and CEO Jeffrey DeBoer, below, said, “Improving and expanding housing affordability is a goal we all share, and any illegal or unjust actions by landlords should not be tolerated. However, this legislation is a short-sighted proposal that will drive up housing costs for working Americans, reduce property values for existing homeowners, and further discourage new home construction.”

- “The bill deflects attention from the real, underlying causes contributing to high housing costs: inflation, labor shortages, and supply chain challenges; rising interest rates and tight credit conditions; NIMBY’ism, discriminatory zoning rules, and restrictive land-use policies; and insufficient investment in the low-income housing credit, to name just a few. Many of these factors are deep, structural challenges. Institutional investors are a convenient scapegoat and a distraction from the real work that must be done to address housing affordability,” DeBoer added.

- By denying basic business expense deductions, the Stop Predatory Investing Act would distort housing markets and create additional, restrictive policies that exacerbate the current supply/demand imbalance.

- Depreciation ensures that the cost of a capital investment is reflected in the measurement of income and recovered, for tax purposes, over the economic life of the investment. Depreciation deductions compensate property owners for the normal wear and tear that reduces the value of a structure over time. Interest expense deductions ensure that taxable income properly takes into account the cost of borrowing to invest in a trade or business.

- Depreciation and interest expense deductions are not “tax breaks” as suggested by the bill’s sponsors. (Senate Banking one-page summary)

House Tax Legislation

- Tax legislation advanced by the House Ways and Means Committee in June is unlikely to receive a vote before Congress starts its August recess.

- House Majority Leader Steve Scalise (R-LA), above, noted this week that the appropriations bills and reauthorization of the National Defense Authorization Act (NDAA), passed today in the House, are the chamber’s current priorities. “Getting the NDAA done and getting the appropriations bills are what are front and center right now. Then, we’ll really look forward to getting that economic agenda moving forward,” Scalise said. (Bloomberg Law, July 12)

- Republican Ways and Means Committee members last month approved their proposed tax legislative package along party lines, including measures on business interest deductibility, bonus depreciation, and opportunity zones. (Tax Notes, June 14 | Ways and Means Committee, June 13 and Roundtable Weekly, June 9)

Scalise added that Ways and Means Committee Chairman Jason Smith (R-MO) is still “working with other members on remaining issues with that bill.” (Bloomberg Law, July 12)

# # #

Roundtable Comments on Clean Energy Tax Credits for Low-Income Communities, Housing

The Real Estate Roundtable submitted comments today on a proposed rule from the IRS and Treasury Department regarding “bonus” tax credits for renewable energy investments in low-income communities, passed by Congress as part of the Inflation Reduction Act (IRA). (Roundtable Comment Letter, June 30)

Solar, Wind Bonus Credits

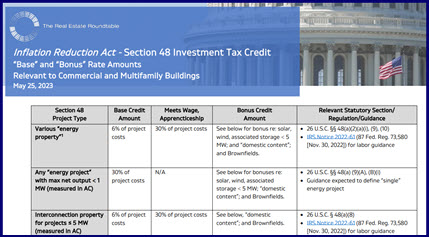

- IRA Section 48(e) establishes a Low-Income Communities Bonus Credit Program to address climate, affordable housing, and environmental justice challenges. (Treasury news release, Feb. 13, 2023)

- Taxpayers must apply to the IRS through a competitive process to receive any bonus credits under the Program.

- The bonus can provide extra tax credits to help cover the costs of solar, wind, and storage facilities. See The Roundtable’s chart, “Base” and “Bonus Rate” Amounts Relevant to Commercial and Multifamily Buildings (May 25, 2023).

- Taxpayers who qualify can layer an extra 10% bonus—above “base rate” credit amounts—for renewable projects in low-income communities defined in the IRA as census tracts that qualify for new markets tax credits.

- The bonus can increase to an extra 20% for clean energy investments that are part of low-income rental housing—such as housing supported by LIHTCs or Section 8 “housing choice” vouchers.

Roundtable Comments

- Treasury and IRS proposed a rule on June 1 to implement the low-income bonus program. Today’s comments from The Roundtable seek greater clarity and certainty for building owners that may access the bonus credits, raising the following points:

- The bonuses are available only for solar or wind projects that generate under 5 megawatts of electrical output. The Roundtable requested a more straightforward rule for what constitutes a “single project” for purposes of this output threshold.

- The IRA’s text requires that multifamily building owners must share “financial benefits” of renewable energy produced on-site with tenants. The Roundtable’s comments stressed that any such benefits should not depend on utility bill savings that accrue directly to tenants—because owners cannot measure, track or control energy consumption in sub-metered leased units.

- Low-income housing supported by non-federal programs through state- and local-level housing finance agencies or public housing authorities should also be eligible for the IRA’s low-income bonuses.

- The proposed rule would offer a preference, not based in the statute, for non-profit owners to receive bonus credit allocations. The Roundtable’s comments urge there should be no bias against business taxpayers to receive the bonus to further the Biden administration’s climate policy goals for rapid deployment of renewable energy investments in low-income communities.

- The bonuses are available only for solar or wind projects that generate under 5 megawatts of electrical output. The Roundtable requested a more straightforward rule for what constitutes a “single project” for purposes of this output threshold.

- Future Roundtable comments on IRA topics are in the works. Feedback on a proposed rule to buy-and-sell certain clean energy credits is due August 14. In addition, proposed rules to implement the 179D tax deduction for energy efficient retrofits of commercial buildings are expected this summer.

Prior comments, information and summaries on The Roundtable’s advocacy efforts regarding clean energy tax incentives are available on our Inflation Reduction Act resources page and in Roundtable Weekly (Dec. 2, 2022 and Nov. 4, 2022).

# # #

Bipartisan Bill Would Correct Condo Construction Tax Accounting Rules and Facilitate Construction Financing

House Ways and Means Committee members Bill Pascrell Jr. (D-NJ) and Vern Buchanan (R-FL) this week reintroduced the Fair Accounting for Condominium Construction Act (H.R. 4280) to correct current condominium tax accounting rules that hamper construction financing.

Discriminatory Tax

- Current condo tax accounting rules require multifamily developers of condominium buildings to recognize income and pay tax on their expected profit as construction is ongoing. This “percentage-of-completion method” requires payment on pre-sale transactions well before a buyer closes and pays for a transaction.

- Homebuilders of single-family homes, townhouses and row houses are not subject to this tax accounting rule restriction, which unfairly accelerates federal income tax liability for new condominium construction.

- The Buchanan-Pascrell legislation would correct the discriminatory tax by providing condominium developers an exclusion from the percentage-of-completion tax method.

Roundtable Support for Change

- Real Estate Roundtable President and CEO Jeffrey DeBoer said, “Developers seeking construction loans face severe headwinds in today’s economy. Our tax accounting rules should not create additional barriers to the financing of new housing construction. Unfortunately, a quirk in the way that federal tax law works accelerates income from the pre-sale of condominium units and prevents developers from using their own revenue to finance condo construction.”

- “This tax aberration is unique to vertical condo development and does not apply to the construction of townhouses, row houses, or buildings with four or fewer units,” DeBoer continued. “The Buchanan-Pascrell bill would fix this issue and allow taxpayers to put their own capital to work expanding the supply and availability of housing.”

- The Roundtable is a long-standing advocate to correct this discriminatory rule as developers have struggled to access their own income (condo pre-sales) to self-finance new construction.

- On August 21, 2019 The Roundtable wrote to former Treasury Secretary Steven Mnuchin requesting regulatory relief from existing tax accounting rules that unfairly accelerate federal income tax liability for new condominium construction. (Roundtable letter)

- The Roundtable’s letter detailed how the completed contract method of accounting— rather than the percentage- of-completion method—would more accurately fit the economics of condominium construction. (Tax Notes, August 23, 2019)

- In 2008, the IRS and Treasury released proposed regulations (REG-120844-07) under section 460 that would treat individual condo units as townhouses or row houses.

The Roundtable’s Tax Policy Advisory Committee (TPAC) continues to advocate for the passage of corrective legislation that would level the playing field for accounting rules impacting condominium construction.

# # #

House Republicans Advance Tax Package, Biden Administration Proposes Rules for Energy Tax Credits

Republican members of the House Ways and Means Committee approved their proposed tax legislative package along party lines this week, including measures on business interest deductibility, bonus depreciation, and opportunity zones. (Tax Notes, June 14 | Ways and Means Committee, June 13 and Roundtable Weekly, June 9)

Tax Measures and CRE

- On Wednesday, Ways and Means Committee Chairman Jason Smith (R-MO), Committee Member Brad Schneider (D-IL), and Ways and Means staff spoke with Roundtable Members about the tax measures and other issues at The Roundtable’s all-member Annual Meeting in Washington, DC during the Tax Policy Advisory Committee (TPAC) session. [Photo left to right: Roundtable Chair John Fish (Chairman and CEO, SUFFOLK), Roundtable President and CEO Jeffrey DeBoer, and Committee Chairman Jason Smith]

- The three tax bills sent to the House floor for a potential vote next week contain $237 billion in business and individual tax cuts, financed by the repeal or modification of several energy tax incentives enacted in last year’s Inflation Reduction Act (IRA). However, differences in the GOP caucus and requests from some Republicans to include a boost in the $10,000 deduction cap on state and local taxes (SALT) could push a vote until after the congressional July 4 recess. Any Republican tax package passing the House would face significant opposition in the Democrat-controlled Senate and the White House. (Tax Notes, June 16)

- The committee’s proposals relevant to real estate include:

- Business interest deduction. The Build It in America Act would provide a 4-year extension (through 2025) of certain, taxpayer-favorable business interest deductibility rules that applied from 2018-2021. The proposal would allow more real estate businesses to operate under the general rules of section 163(j) and its preferable cost recovery schedules. (H.R. 3938 and summary)

- Bonus depreciation. H.R. 3938 also includes a 3-year extension (through 2025) of 100% bonus depreciation for qualifying capital investments, including equipment, machinery, and interior improvements to nonresidential property (“qualified improvement property”). Bonus depreciation is 80% in 2023 and gradually phasing down.

- Opportunity Zones. The Small Business Jobs Act would establish special, favorable rules for investments in rural opportunity zones. It would also create a new and detailed information-reporting regime for all opportunity funds. (H.R. 3937 and summary)

Energy Tax Credits Transferability

- The Biden administration this week proposed rules on transferring clean-energy tax credits under the IRA. Treasury’s proposed guidance released on June 14 seeks to clarify numerous issues, including which entities would be eligible for each credit monetization mechanism, laying out the process and timeline to claim and receive an elective payment, and transferring a credit. (Tax Notes, June 15 |The Wall Street Journal, June 14 | IRS news release)

- Secretary of the Treasury Janet Yellen stated, “The Inflation Reduction Act’s new tools to access clean energy tax credits are a catalyst for meeting President Biden’s historic economic and climate goals. They will act as a force multiplier, bringing governments and nonprofits to the table.” (CNBC and Treasury news release, June 14)

- The Roundtable’s Tax Policy Advisory Committee (TPAC) and Sustainability Tax Policy Committee (SPAC) will analyze the impact of the transferability rules on commercial real estate for potential comments on the proposed rulemaking. SPAC’s meeting on Wednesday during The Roundtable’s Annual Meeting included a presentation about an online marketplace for exchanging such tax credits.

Climate Disclosure Regs![]()

- Separately, the Securities and Exchange Commission (SEC) expects to issue new climate disclosure rules by October, a year later than the original target date. The new date was included in a SEC rule-making agenda and schedule released on Tuesday.

- Legislation to constrain future SEC disclosure requirements was reintroduced this week by Sen. Mike Rounds (R-SD) and nine of his Senate colleagues. The bill includes language stating that an “issuer is only required to disclose information in response to disclosure obligation adopted by the Commission to the extent the issuer has determined that such information is important with respect to a voting or investment decision regarding such issuer.” Rep. Bill Huizenga (R-MI) is sponsoring a version of the bill in the House. (Sen. Rounds news release and Politico Pro, June 15)

The Roundtable’s SPAC will continue to track any developments related to the SEC’s forthcoming rule on climate reporting, including its proposal for sweeping disclosures on Scope 3 GHG emissions affecting CRE. (Roundtable Weekly, March 10)

# # #

House Republicans Unveil Tax Package; Ways and Means Chairman to Address Real Estate Roundtable Next Week

The House Ways and Means Committee unveiled a tax package today that includes measures impacting commercial real estate, and announced a legislative mark-up on June 13. (Politico and Tax Notes, June 9)

Committee Chairman Jason Smith (R-MO), above, Ways and Means Member Brad Schneider (D-IL), and committee staff will speak on June 14 during The Roundtable’s all-member Annual Meeting in Washington, DC at the Tax Policy Advisory Committee (TPAC) meeting.

GOP Proposal & CRE

- Chairman Smith released a statement today about the package, which includes the following bills scheduled for markup next week:

- The proposals relevant to real estate include:

- Business interest deduction. The Build It in America Act (H.R. 3938) would provide a 4-year extension (through 2025) of certain, taxpayer-favorable business interest deductibility rules that applied from 2018-2021. The proposal would allow more real estate businesses to operate under the general rules of section 163(j) and its preferable cost recovery schedules.

- Bonus depreciation. H.R. 3938 also includes a 3-year extension (through 2025) of 100% bonus depreciation for qualifying capital investments, including equipment, machinery, and interior improvements to nonresidential property (“qualified improvement property”). Bonus depreciation is 80% in 2023 and gradually phasing down.

- Opportunity Zones. The Small Business Jobs Act (H.R. 3937) would establish special, favorable rules for investments in rural opportunity zones. It would also create a new and detailed information-reporting regime for all opportunity funds.

- The GOP package (H.R. 3938) also contains proposals that would repeal some clean energy provisions from the Inflation Reduction Act (H.R. 5376), including electric vehicle tax credits, clean energy production, and investment tax credits.

Prospects for Passage

- The Ways and Means proposal may pass through committee—and possibly pass the Republican-majority House—but such a package faces steep obstacles in the Democrat-controlled Senate and with the White House.

The proposals are a good indication of the priorities that House Republicans will bring to any bipartisan economic policy negotiations as the year unfolds.

# # #

Debt Ceiling Compromise Passed Days Before National Default Deadline

Congress passed compromise legislation this week to suspend the debt ceiling for two years and restrain government spending, sending it to President Biden for his signature and calming world financial markets days before a US government default. (CQ and Wall Street Journal, June 2)

After the Debt Ceiling

- The House on Wednesday night passed the Fiscal Responsibility Act (H.R. 3746)—forged by President Joe Biden, House Speaker Kevin McCarthy (R-CA), and their negotiation teams—to suspend the nation’s $31.4 trillion debt limit until Jan. 1, 2025 and cut spending by at least $1.5 trillion. The Senate approved the bill last night by a bipartisan vote of 63-36. (Congressional Budget Office, May 30 and Associated Press, May 26)

- “No one gets everything they want in a negotiation, but make no mistake: this bipartisan agreement is a big win for our economy and the American people,” President Biden stated last night. “I look forward to signing this bill into law as soon as possible…” (White House statement, June 1)

- House policymakers have signaled they may follow the debt ceiling crisis with a legislative tax proposal that could include significant measures affecting commercial real estate. (Roundtable Weekly, May 26)

- Congressional action on such measures would come at a time when the office sector faces difficult conditions, including asset price discovery and tighter liquidity. (Wall Street Journal, May 30 Financial Times, May 29 | GlobeSt, May 26)

Economic Conditions & CRE

- Real Estate Roundtable Chair John Fish (Chairman and CEO, SUFFOLK) explained the economic conditions facing CRE and the office market, along with other pressures such as remote work and a shortage of labor, in a May 26 Boston Globe interview. “We’re in a very precarious situation,” Fish said.

- Roundtable Board Member Ross Perot, Jr., above, (Chairman, The Perot Companies and Hillwood) discussed the financing challenges faced by some CRE sectors in an interview with Bloomberg TV on Wednesday. “If the industry can’t get a construction loan, real estate will have a recession,” Perot said. “The key to commercial real estate today will be banking.”

- The Federal Reserve’s “Beige Book” issued this week also reported on the nation’s current overall economic activity, noting, “Commercial construction and real estate activity decreased overall, with the office segment continuing to be a weak spot.” (GlobeSt, May 31)

- Additionally, Trepp’s CMBS Delinquency Report issued this week showed the nation’s overall CMBS delinquency rate hit a 14-month high, topping 4% for the first time since 2018. Although May’s delinquency rate jumped to 3.62%, up 53 basis points for the month, the all-time high registered 10.34% in July 2012 and the COVID-19 high reached 10.32% in June 2020.

- Federal Reserve monetary policies, congressional fiscal policy, potential tax measures, and other issues impacting CRE will be discussed during The Real Estate Roundtable’s Annual Meeting on June 13-14 in Washington, DC.

The Roundtable meeting includes policy advisory committee meetings—open to all members—that will feature prominent policymakers, including Senate Banking Committee Member Bill Hagerty (R-TN); House Ways and Means Committee Chairman Jason Smith (R-MO); David Crane, the US-DOE’s Director of the Office of Clean Energy Demonstrations; and Alejandra Nunez, US-EPA Assistant Administrator overseeing climate policy.

# # #

Bipartisan Legislation Reintroduced to Allow Greater REIT Equity Investments in Distressed Retail Tenants

Bipartisan legislation reintroduced this week by House Ways and Means Committee Members Darin LaHood (R- IL) and Brad Schneider (D-IL) would allow real estate investment trusts (REITs) to make greater equity investments in retail tenants that have yet to recover from the pandemic’s economic impact.

Support for Retail Tenant Assistance

- The Retail Revitalization Act (H.R. 3749) is aimed at unlocking capital for productive investment and helping prevent further large-scale job losses and bankruptcies in the retail sector and its supply chain. (Congressional Record, May 30)

- As of May 5, ten major retailers had filed for bankruptcy protection in 2023. The number of retail failures, which includes Bed Bath & Beyond, David’s Bridal, and Party City, is already twice the level of 2022. More bankruptcies are anticipated. (Forbes, May 5 and Forbes, May 15)

- Real Estate Roundtable President Jeffrey DeBoer stated, “The Retail Revitalization Act would reform an outdated section of our tax code that currently prevents the commercial real estate industry from stepping forward and deploying its own capital to solve significant economic challenges. Retail bankruptcies have negative consequences for employees, surrounding businesses, and local communities. This bipartisan legislation to allow REITs to invest more heavily in their tenants is exactly the type of cost-effective, commonsense measure that everyone can and should support. The bill will save jobs, increase local tax revenue, and create a stronger foundation for future economic growth.”

Amending REIT Rules

- The LaHood-Schneider legislation—strongly supported by The Real Estate Roundtable—would modify tax provisions limiting REITs’ ability to invest equity capital in their retail tenants. The bill would amend existing “related-party rent” rules by:

- increasing the capacity of a REIT to own the equity of a distressed tenant from 10% to 50% and from 10% to 30% for all other tenants;

- changing the ownership attribution rules used to determine what is considered related party rent under current REIT rules to the general ownership attribution rules used elsewhere in the tax code, and;

- changing the limitation on space that a REIT can lease to its taxable REIT subsidiary.

Tax Policymakers

Tax proposals such as H.R. 3749 and others will be discussed during TPAC, held in conjunction with The Roundtable’s all-member Annual Meeting on June 13-14 in Washington, DC. TPAC speakers will include:

Tax proposals such as H.R. 3749 and others will be discussed during TPAC, held in conjunction with The Roundtable’s all-member Annual Meeting on June 13-14 in Washington, DC. TPAC speakers will include:

- House Ways and Means Committee Chairman Jason Smith (R-MO), above

- House Ways and Means Committee Member Brad Schneider (D-IL)

- Joint Committee on Taxation Chief of Staff Thomas Barthold

- Senior staff from Senate Finance Committee and House Ways and Means Committee

TPAC will also feature a panel session on “Post-Pandemic Real Estate Challenges and Tax Policy: Debt Workouts / Tax Incentives for Property Repurposing, Community Revitalization, and Housing.” All Roundtable members are encouraged to attend.

# # #

House Tax Package Expected to Follow Debt Ceiling Resolution

The House Ways and Means Committee may release a tax-focused economic growth package in June after a final resolution is reached between President Joe Biden, House Speaker Kevin McCarthy (R-CA), and their negotiation teams on the debt ceiling. The intense talks on federal spending limits have less than a week before the Treasury Department estimates the nation may default on its debt obligations. (Wall Street Journal, May 25 | PoliticoPro, May 23 | Roundtable Weekly, May 19)

The House Ways and Means Committee may release a tax-focused economic growth package in June after a final resolution is reached between President Joe Biden, House Speaker Kevin McCarthy (R-CA), and their negotiation teams on the debt ceiling. The intense talks on federal spending limits have less than a week before the Treasury Department estimates the nation may default on its debt obligations. (Wall Street Journal, May 25 | PoliticoPro, May 23 | Roundtable Weekly, May 19)

Tax Measures & CRE

- The House Republican tax package is about 90% complete and “buttoned up pretty tight,” according to Ways and Means Member Kevin Hern (R-OK). “We’re making sure that we don’t disrupt any of the debt limit conversations and distract from that, but it would be ready to go very quickly,” Hern said. (Tax Notes, May 24)

- Ways and Means Committee Member Randy Feenstra (R-IA) commented that the package will likely include measures that expired last year, including full bonus depreciation and certain taxpayer-favorable rules related to the deductibility of business interest under Section 163(j)—both supported by The Real Estate Roundtable. (PoliticoPro, May 23 and BGov, May 25)

- Under the Tax Cuts and Jobs Act (TCJA) of 2017, 100% bonus depreciation applies to capital investments made between 2018 and 2022 (as well as capital improvements made to the interior of nonresidential buildings). However, the bonus depreciation benefit began phasing down this year. In addition, real estate businesses that elect out of TCJA’s limits on business interest deductibility do not qualify for the bonus depreciation benefit.

- The House tax package is expected to extend 100% bonus depreciation through at least 2025, allowing many taxpayers to continue immediately expensing qualified interior improvements. Moreover, by reinstating certain expired provisions from section 163(j), the tax bill would allow more real estate businesses to avail themselves of the bonus depreciation benefit without inhibiting their ability to deduct their business interest expense.

Additional Provisions and TCJA Permanency

- The economic growth package could also include provisions extending the enhanced child tax credit and the deductibility of R&D expenditures. Housing-related measures, such as an expansion of the low-income housing tax credit, are also under consideration.

- Separately, the Ways and Means Committee may also consider the TCJA Permanency Act (H.R. 976), reintroduced by Committee Vice Chairman Vern Buchanan (R-FL) in February. The bill would permanently extend TCJA provisions scheduled to sunset at the end of 2025, including the 20 percent deduction for qualified pass-through business income (Section 199A). (Tax Notes and Roundtable Weekly, Feb. 24)

- While a TCJA permanency bill is likely dead on arrival in the current Senate, the House economic growth tax package could be the starting point for bipartisan negotiations with congressional Democrats on a limited number of tax and economic priorities as the year further unfolds.

House Ways and Means Committee Chairman Jason Smith (R-MO) will be a guest at The Roundtable’s June 13-14 all-member Annual Meeting and policy adivisory committee meetings will include discussions on a debt ceiling agreement and potential tax legislation.

# # #

Senate Republican Taxwriter Introduces Legislation to Permanently Extend 20% Pass-Through Income Deduction

Yesterday, Senate Finance Committee member Steve Daines (R-MT) reintroduced legislation to make permanent the 20 percent deduction for pass-through business income (Section 199A), one of the cornerstone provisions of the Tax Cuts and Jobs Act of 2017 that expires at the end of 2025.

Deduction Sunset

- The Main Street Tax Certainty Act of 2023 supports small businesses, helps create jobs, and strengthens the economy. (Sen. Daines’ news release, May 18)

- House Ways and Means Committee Chairman Jason Smith (R-MO), who has long championed making Section 199A permanent, is anticipated to re-introduce the legislation in the House soon.

- In 2017, Congress created the 20% deduction for pass-through business income to avoid putting businesses organized as partnerships, S corporations (S corps), and real estate investment trusts (REITs) at a competitive disadvantage relative to large C corporations (C corps).

- Section 199A is scheduled to sunset on Dec. 31, 2025 as businesses continue to recover from post-pandemic price hikes, labor shortages, and supply chain disruptions.

Section 199A Permanency

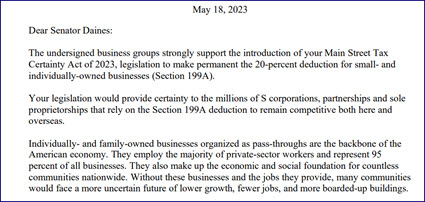

- The Real Estate Roundtable and a coalition of more than 145 business organizations sent a letter yesterday to Sen. Daines in support of the bill. (Coalition letter, May 18)

- The letter notes that the bill “would provide certainty to the millions of S corporations, partnerships and sole proprietorships that rely on the Section 199A deduction to remain competitive both here and overseas.”

- Previously, The Roundtable and other stakeholders supported congressional efforts in 2021 to make the pass-through deduction permanent. (Coalition letter, Feb. 26, 2021 and Tax Notes, March 1, 2021)

While House Republicans are expected to introduce an economic growth package in the coming weeks that includes tax cuts, it is unclear whether the bill will address provisions such as Section 199A that are not scheduled to expire until the end of 2025.

# # #