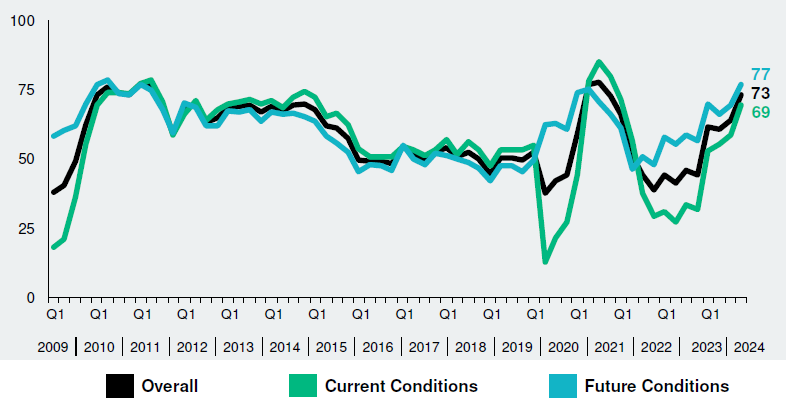

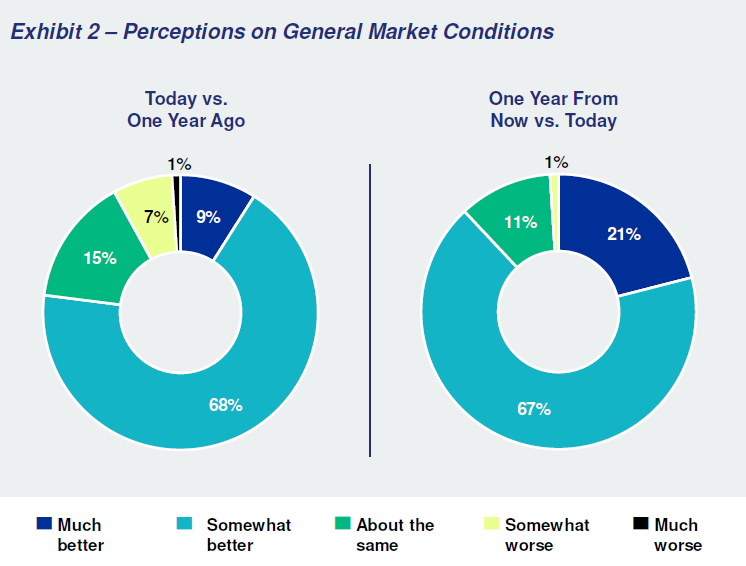

The commercial real estate sector is at a critical inflection point, with numerous positive indicators signaling substantial progress on recovery and growth since the pandemic’s initial disruption to the industry.

Key factors driving the change are easing interest rates, continued return-to-office momentum, property conversions and rising office demand from tech and AI sectors, though some challenges remain.

Driving Factors in CRE’s Recovery

- Interest rates have continued to ease, with the Federal Reserve cutting rates by another 0.25 percentage points last week. While inflation has shown some lingering signs of persistence, Fed Chair Jerome Powell indicated that interest rates are likely to continue to come down slowly and deliberately in the coming months. (Roundtable Weekly, Nov. 8, AP, Nov. 14)

- CRE lending has also improved, with buyers and owners taking advantage of lower interest rates. Total commercial and multifamily originations increased by 59% year-over-year across many property types including healthcare, retail, multifamily and industrial, though office lending remains relatively stagnant. (GlobeSt, Nov. 12) (Bisnow, Nov. 11)

- Office leasing has seen an uptick, with several major brokers, including JLL and CBRE, reporting significant increases in office leasing revenue. Larger lease sizes and a rising return-to-office trend have been key contributors, with the average number of in-office days required per week by employers up 50% compared to last year. (CoStar, Nov. 11)

- Regional office visit data indicates that October 2024 was the busiest in-office month since the pandemic for major hubs like Atlanta, Dallas, Houston, Denver, Washington, D.C., Chicago, and San Francisco. (GlobeSt., Nov. 15)

- Office leasing has been further buoyed by growing demand from tech and AI companies. Tech firms leased 9.9 million square feet of U.S. office space during the third quarter, the highest level in nearly three years—supporting activity in high-value office locations such as San Francisco, Seattle, and New York. (WSJ, Nov. 12)

Property Conversions

- Property conversions have been a bright spot in 2024, with 73 projects already completed this year and another 30 scheduled to be completed by year-end.

- The vast majority are office-to-residential conversions—71 million sq. ft., or 1.7%, of U.S. office inventory was planned for or already undergoing conversion, helping to increase the supply of housing, boost downtown vibrancy and ease office vacancy rates. (CBRE, Nov. 11)

What’s Next: RER’s Real Estate Capital Policy Advisory Committee (RECPAC) will be meeting in person next week on November 19, 2024 in New York to discuss the economic outlook, capital and debt markets and much more.